U.S. ECONOMIC MACRO COMMENTARY & INSIGHTS

- New-home sales slump to slowest pace since November

- Mortgage rates remain elevated

- Prices climb to new highs amid low inventory

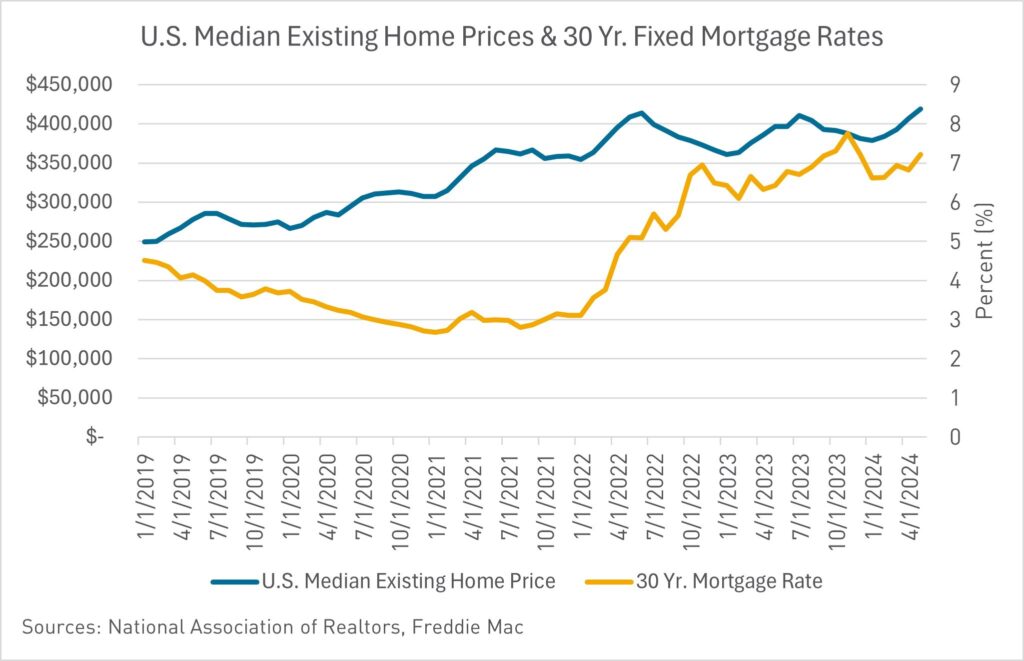

Beyond Insights reported last year that the United States’ single-family housing market had hit the least affordable point seen in decades. Since that report, the market has only gotten less affordable. The National Association of Realtors (NAR) reported that the median existing-home price for all housing types in May was $419,300, the highest price ever recorded and an increase of 5.8% from one year ago. Interest rates have rallied off recent highs; however, higher home prices have negated the slightly lower interest rates, and monthly payments on a new 30-year fixed-rate mortgage are now at all-time highs. The average monthly mortgage payment required on an entry-level home has reached the point where potential first-time buyers are delaying home purchases and increasingly focusing on affordable rental opportunities. Average rent is significantly lower than the average mortgage payment, and affordable units are more widely available. Single-family rentals are also an increasing percentage of the market, providing renters with more choices than they previously had.

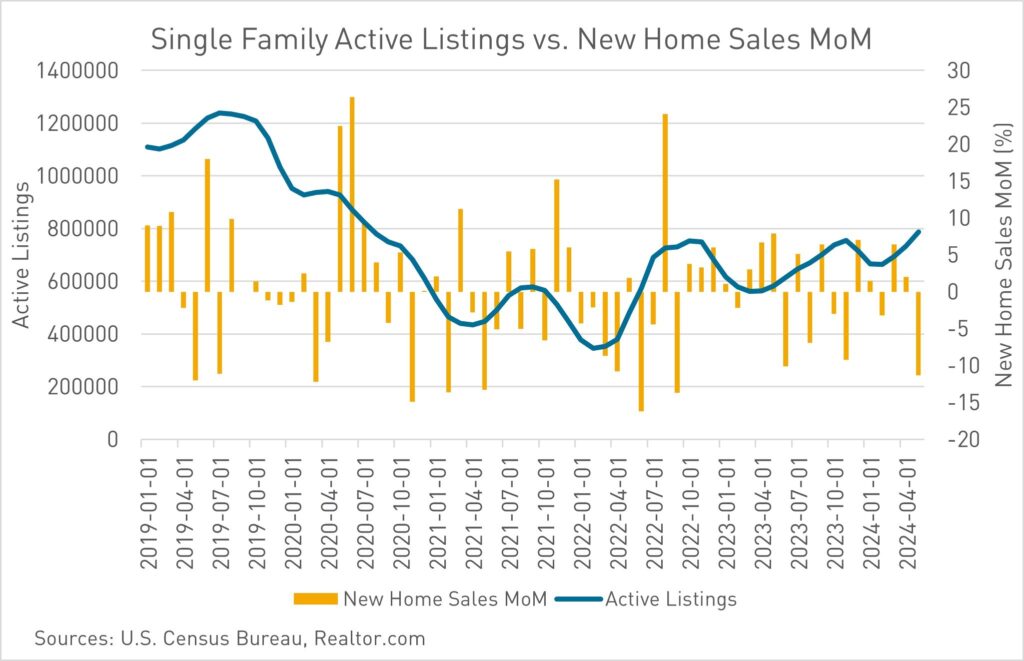

High prices, paired with elevated mortgage rates, have limited the number of sales this spring—typically the busiest season for home buying. The U.S. Census Bureau reported on Wednesday that sales of new single-family homes fell 11.3% from the previous month to a seasonally adjusted rate of 619,000, a six-month low. On an annual basis, sales plunged 16.5%. Low housing inventory continues to spur bidding wars among home buyers in some markets. Sales of previously owned homes decreased 0.7% from the prior month to a seasonally adjusted annual rate of 4.11 million, the third straight monthly decline, NAR said. On an annual basis, existing-home sales, which make up most of the housing market, fell 2.8%.

To further exacerbate the imbalance of supply and demand in the housing market, data from the U.S. Census Bureau shows that housing starts have sunk to their lowest point since the early days of the pandemic in 2020, recording a 19% drop compared to last year. With the Federal Reserve holding posture in their “higher for longer” interest rate policy, the downturn in the housing market is intensifying, impacting both builders and prospective homeowners. Housing starts fell 5.5% from April to a seasonally adjusted rate of 1.277 million. This print was a miss to market expectations of a rise to an annual rate of 1.37 million. “Overall lower housing production corresponds with our latest industry surveys, which show builders are concerned with a high interest environment that is making it harder to get acquisition, development and construction loans to increase home building activity,” National Association of Home Builders (NAHB) chairman Carl Harris said in the news release. “Higher rates for builder and developer loans, along with ongoing supply-side challenges regarding construction labor and buildable lots, are acting as headwinds for new home construction.”

The underlying issue causing the minimal transaction volume in the single-family housing market is the delta between today’s interest rate and the interest rates available in 2020 through 2022. Mortgage rates throughout the Covid-19 pandemic hovered around 3%. Approximately one-third of outstanding mortgage balances were refinanced during the seven quarters of this refinance boom, and an additional 17% of mortgages outstanding were refreshed through home sales during a time of high demand for housing. According to Freddie Mac’s Primary Market Mortgage Rate Survey, the 30-year fixed-rate mortgage averaged 3.0% in 2021. In 2021, there were about $2.8 trillion in first-lien refinance originations, a 7.6% decline from 2020. Homeowners who are locked into a low-interest-rate mortgage are hesitant to move due to the drastic increase in the monthly payment they would pay on a new mortgage.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.