Economy

From interest rates to inflation, understand the impact of macroeconomic trends on the real estate capital markets.

The Beyond Insights series aims to deliver timely economic and market-driven insights to better inform your commercial real estate investment decisions.

Markets

From local market rents to cap rates, catch up on the latest capital markets insights.

Learn moreU.S. ECONOMIC MACRO COMMENTARY & INSIGHTS

The Market Tightened for Warsh. Now What?

- Markets priced the hike even though the Fed didn’t deliver one.

- Warsh argued higher yields already did some of the Fed’s work.

- Softer inflation data buys time, but not unlimited credibility

Markets came into Wednesday’s FOMC meeting focused on one question: why didn’t the Fed raise rates? Warsh seemed focused on a different one entirely: how much tightening had already occurred since the last meeting?

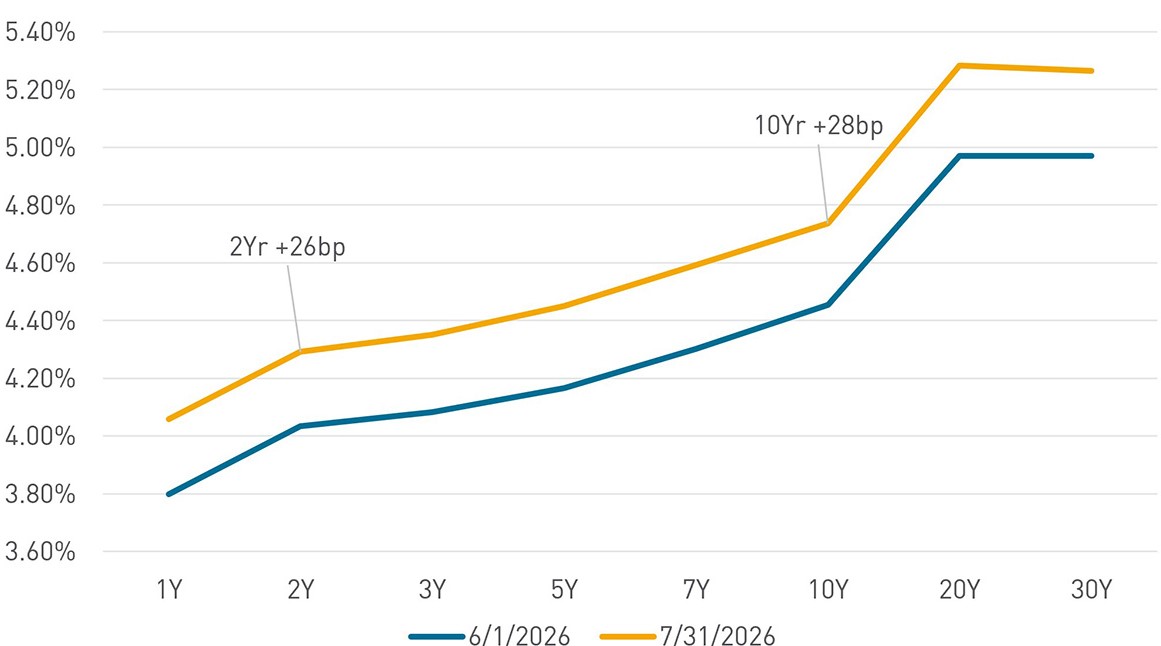

Yield Curve change since june 1

2026 Multifamily Investor Sentiment Survey

In December 2025, we surveyed over 250 of our trusted clients from various companies, with most holding senior-level titles, for our second annual Multifamily Investor Sentiment Survey. Our goal is to provide a comprehensive view of current market sentiments to our clients, and we plan to share our findings in our detailed report.

2026 Multifamily

Powerhouse Poll

In Berkadia’s Annual Multifamily Powerhouse Poll, we surveyed over 200 investment sales advisors and mortgage bankers to offer their unique perspectives on the state of the commercial real estate (CRE) industry.

The Market Tightened for Warsh. Now What?

A hawkish Fed Chair, softer inflation data, and a credibility test arriving sooner than the market may expect. Markets came into Wednesday’s FOMC meeting focused on one question: why didn’t the Fed raise rates? Warsh seemed focused on a different one entirely: how much tightening had already occurred since the last meeting? The FOMC voted…

Labor Market Cools, but Inflation Remains the Bigger Problem

After three consecutive months of stronger-than-expected payroll growth, June finally delivered a downside surprise. Employers added just 57,000 jobs during the month and prior months were revised lower, taking some of the shine off what had looked like a meaningful reacceleration in hiring. Headline unemployment rate improved to 4.2%, but the details were less encouraging.…

The Missing Dot

Everyone will focus on the missing dot. The market sold off because of the nine that remained. Half the committee is now willing to discuss another rate hike this year, and that is a very different conversation than the one markets were having just a few months ago. Inflation forecasts moved higher, growth forecasts moved…