U.S. ECONOMIC MACRO COMMENTARY & INSIGHTS

- Weak economic data or the carry trade: is it a chicken-or-egg scenario?

- Slowing inflation data providing support for the rate cut cycle

- Futures market still overplaying rate cut expectations for this year

The first Friday of every month generally has financial analysts of all stripes waiting for 8:30 AM, when we get a slew of important releases—most notably the Nonfarm Payrolls (NFP) and Unemployment Rate reports. On the first Friday in August, we had a surprise miss to the downside on NFP, with only 114K jobs being added, and the unemployment rate unexpectedly ticking up to 4.30%, the highest since the COVID pandemic days. What ensued over the next two business days was mayhem: the Dow dropping 1,000 points overnight, Nasdaq plummeting, and Treasury yields across the curve tanking. With the benefit of a couple weeks of hindsight, we can see that while the U.S. economic data may have been the smoke, the fire was elsewhere.

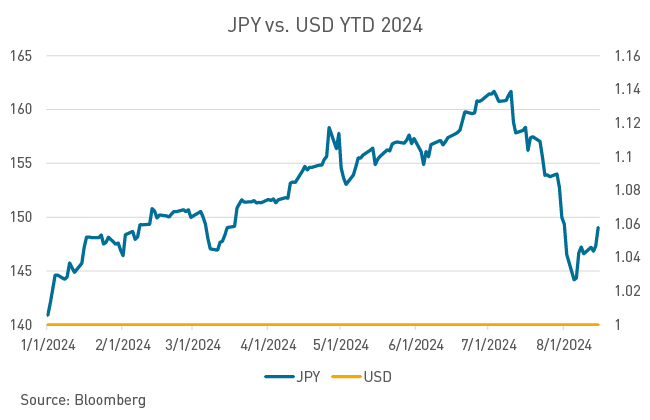

Enter the carry trade. At its most basic, the carry trade involves borrowing in a low-cost currency to invest in assets or other currencies offering higher yields. As long as you make more than your debt costs, and the borrowed currency is stable relative to the currency you’re using to buy assets, you make money. Thanks to a long-standing policy of the Bank of Japan, the yen has had ultra-low interest rates and carried a stable value relative to the dollar. With the American share of the world’s stock market capitalization sitting at around 61% (despite only being just over a quarter of global Gross Domestic Product) and U.S. equities going on a tear, a significant amount of money was tied up in borrower yen and investing in U.S.-denominated assets.

The carry trade works—until it doesn’t. The Bank of Japan not only hiked its policy rate by more than most had expected but also detailed its intention to shrink the hoard of Japanese government bonds it owns. Coupling the Bank of Japan’s actions with expectations of an impending U.S. Federal Reserve rate cut has caused rapid appreciation of the yen against the U.S. dollar, a 14% increase from July 10 to August 5.

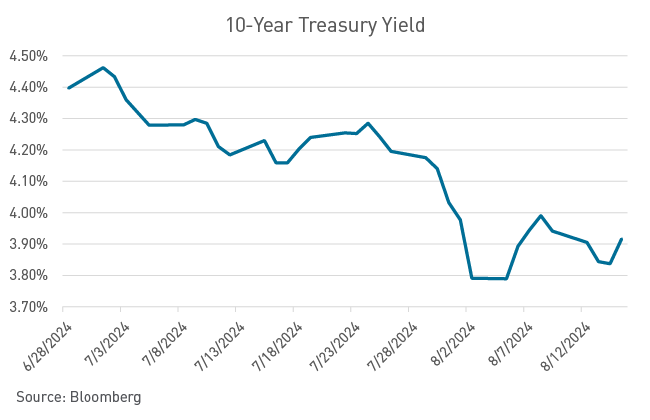

Put another way, any non-yen assets declined in value relative to the yen borrowing costs by as much as 14%. Investors needed to unwind their carry trades or risk being swept away, as this depreciation effectively acted as a global margin call. The global equity rout contributed to a flight to quality, which sent U.S. Treasury yields plummeting.

Since August 6, volatility has felt especially elevated. There were immediate calls for the Federal Reserve to cut rates before their next scheduled meeting, but these were reluctantly dismissed as the market righted itself. However, Wall Street still believes in the “Fed Put”—the idea that the Fed will lower rates if financial markets start to collapse. While the equity volatility index (VIX) has returned to July levels in the immediate aftermath of the carry trade unwind, the MOVE index (the bond market parallel) remains elevated. To point, the 10-year U.S. Treasury (UST) has had greater than a 10-basis-point intraday yield move on 63% of August trading days.

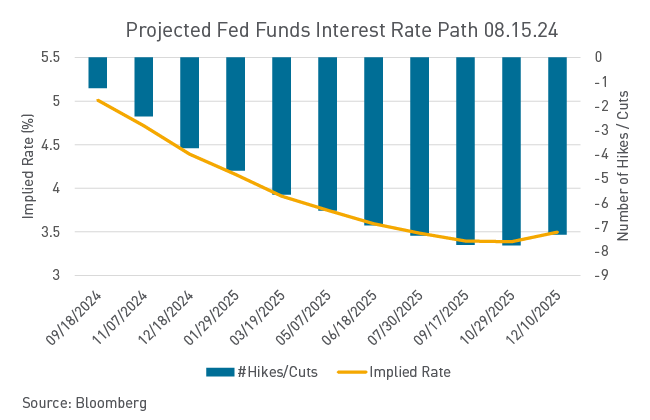

Against this backdrop, we do have mixed messaging in U.S. economic reports. The U.S. Consumer Price Index (CPI) was released this week, and somehow meeting market surveys disappointed the market. The exuberance for rate cuts had gotten ahead of itself, and a weak CPI print would have been the thumbs-up the market was hoping for to price in even more aggressive rate cuts. The ho-hum meets expectations still keeps significant cuts priced into the market but served as a bit of a damp blanket on market enthusiasm, which pared back expectations from five cuts this year to only three.

There was some noise in the July CPI print, most notably in rents, with “rent of primary residence” accelerating significantly, which seems to defy market experience. Still, the weakening economic data does provide friendly cover for the Federal Reserve to start its rate-cutting campaign as early as September. We will still advise caution against the massive rate cut camp, as signs are pointing to a disciplined and patient rate-cutting campaign. While it’s possible that the Fed teases some information at their Jackson Hole Economic Symposium next week, it’s more certain that the bond market will overreact to each data point, and volatility is going to be the main character of the next several weeks.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.