- FOMC unanimously votes to cut rates by 25 bps

- FOMC members see the risks to its dual mandate—price stability and full employment remain “roughly in balance”

- Fed Chair Powell declared that the U.S. presidential election will have “no effects” on the central bank’s policy decisions in the near term

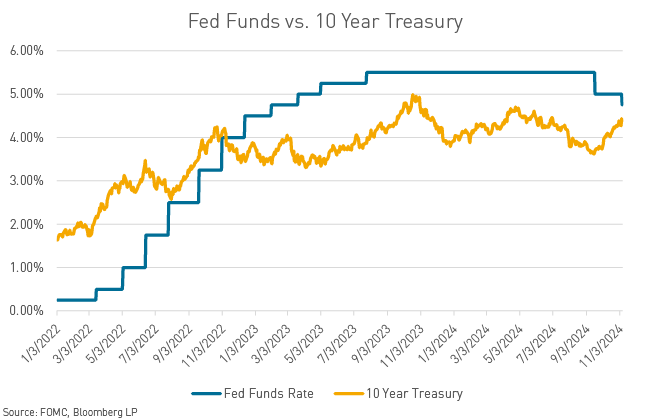

The Federal Open Market Committee (FOMC) held its November meeting on Thursday this week. Committee members unanimously voted to cut rates by 25 basis points, lowering their target rate range to 4.50%–4.75%. The November 25 bp cut was the second move in the Fed’s rate-cutting cycle, following their initial 50 bp cut in September. The Fed’s statement proclaimed that the risks to its dual mandate—price stability and full employment—remain “roughly in balance.” Fed chair Jerome Powell noted at Thursday’s press conference, “This further recalibration of our policy stance will help maintain the strength of the economy and the labor market and will continue to enable further progress on inflation as we move toward a more neutral stance over time.” Powell declared that reducing rates too quickly could hinder progress in getting inflation down, but cutting too slowly “could unduly weaken economic activity and employment.” Powell noted that policy is “well-positioned” to deal with the “risks and uncertainties” the economy faces.

On the heels of a Trump victory in the November presidential election, FOMC members positioned themselves for policy optionality moving forward. When asked what impact the election has on the economic and policy outlook, Powell said that in the near term the election “will have no effect” on Fed decisions. “We don’t know what the timing or substance” of economic policy will change going forward, and the Fed isn’t going to guess or assume what’s going to happen. “We don’t comment on fiscal policy,” he said when asked if expectations for tax cuts are feeding through into the sell-off in Treasuries, but he added that if tax policy does change, those measures would be fed into economic models “along with a million other things” to assess the impact. Powell also notes that tax legislation does take time to make its way through Congress. Only after all that would the Fed stick such factors into its models.

Trump’s victory will certainly require recalibrations to the Fed’s search for the economy’s “neutral rate,” the interest rate that supports the economy at full employment / maximum output while keeping inflation constant. The Fed will continue to leverage labor market prints to determine future policy, and market projections surrounding these prints will surely cause short-term treasury rate volatility. Fed chair Powell was determined not to offer any forward guidance on where he and other officials see rates heading in December or next year, proclaiming that the Fed will continue to leverage the data month by month. Powell noted that rates are “still restrictive” even after today’s cut. If policy is still restrictive, and risks are in balance as the Fed says, then that would argue for further “recalibration,” as Powell puts it. As the Fed gets closer to neutral, it may be appropriate to slow the pace of recalibration, Powell noted. “It’s something that we’re just beginning to think about.” Unprompted, Powell added that officials are thinking about the central bank’s asset runoff, or quantitative tightening. “We reach a point where we slow the pace, much like an airplane reaching the airport slows down,” he said.

Treasury rates increased significantly since the Fed’s first rate cut in September; the 10-year U.S. Treasury (UST) increased over 75 bps between FOMC meetings. Yields have increased in large part because better economic data has somewhat curbed recession worries, which could have triggered larger rate cuts. Powell touched on these financial conditions at the November press conference: “We’re watching that. Things have been moving around, and we’ll see where things settle.” He added that it appears that the movements in rates are not principally about higher inflation expectations but rather more about stronger growth.

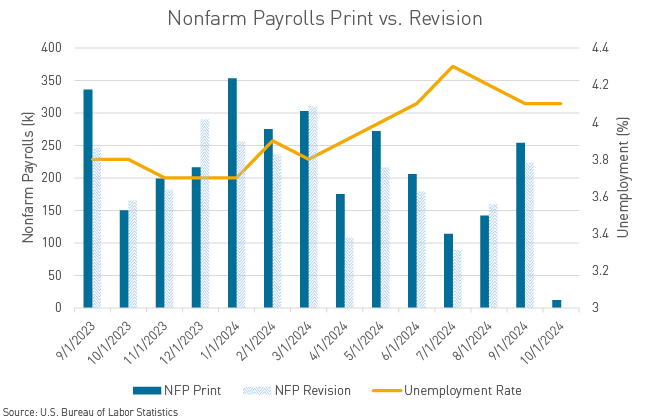

The Fed and the market alike have shrugged off the October nonfarm payrolls print, which showed that job growth slowed significantly last month but was heavily affected by outside factors. The highly anticipated print missed analysts’ expectations, with the economy adding just 12,000 jobs in October, well short of the 100,000 jobs projected by economists. The nonfarm payrolls figure was drastically affected by hurricanes Helene and Milton, as well as the Boeing worker strike. The unemployment rate remained flat to last month’s figure at 4.1%. The Fed tweaked language in its statement to note that “labor market conditions have generally eased,” and repeated that “the unemployment rate has moved up but remains low.”

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.