- Agency CMBS Trading Spreads tightened significantly in November, reaching multiyear tights

- New issuance Agency CMBS is down year over year, curbed by high treasury rates

- Imbalance of supply and demand continues to drive spreads tighter

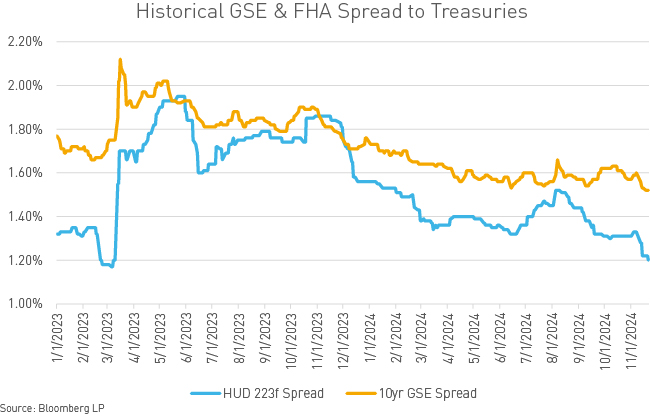

Agency commercial mortgage-backed securities (CMBS) trading spreads are currently at multiyear tight levels; spreads have gapped tighter in November as the market has embraced a risk-on appetite for bonds. Following spread-widening to start the fourth quarter, current MBS levels on 10-year Fannie Mae Delegated Underwriting and Servicing (FNMA DUS) and Freddie Mac K-A2 bonds have reversed course and are currently the tightest seen since February of 2022. Ginnie Mae (GNMA) 223f trading spreads tightened even more significantly than government-sponsored enterprise (GSE) spreads over the course of the month and are now at their tightest level since the regional banking crisis of March 2023. This year’s tightening has been driven by an imbalance of supply and demand, with new issuance for Fannie Mae DUS and Ginnie Mae MBS down significantly year over year, while demand from end accounts is driving spreads tighter.

GNMA project loan spreads have been the darling of the recent tightening cycle; spreads have tightened 12 bps over the course of the month, and nearly 25 bps since the start of the quarter. The supply of new-issuance GNMA loans continues to be low, as high treasury rates make financing deals challenging. The curbed supply has caused the frequency and size of GNMA securitizations to shrink; the count and size of securitizations is at a decade low. With the regional banking crisis finally in the rearview mirror, demand for these securitizations has begun to return to the market. This increased demand, paired with a very low supply of new issuance, has helped drive spreads tighter. Smaller deals of around $10 million that provide diversification without unduly adding size to a securitization as well as deals that utilize a buydown are trading the best, but demand is still strong for larger deals, as undersupply issues remain. Construction loan spreads have followed suit with the tightening of project loan spreads and are generically 35-40 bps wider than a standard project loan.

The past three months have been volatile for FNMA DUS spreads; volatility has been predominantly driven by fluctuations in volume. As the 10-year treasury rate dipped in mid-September to year-to-date (YTD) lows, volume soared. Berkadia’s trading desk tracked over $1 billion in new origination per week in September, and it projects that a vast majority of these bonds will be reflected in the November Fannie Mae issuance number. As this volume saturated the market, spreads gapped wider. This trend was short-lived however, as treasury rates rose over 90 bps from their September lows, and volume flow was trimmed. Weekly new issuance numbers now resemble where they were in the first half of this year.

FNMA DUS has been trading well across tenors, as five-year through 10-year spreads have all tightened in tandem. The rare, longer-term 12-year and 15-year deals trade extraordinarily well in the market, with end accounts jumping on the opportunity to purchase longer-duration paper. Deals that utilize a rate buydown are seeing strong market execution, as buyers are more amenable to the lower coupon and can save an extra couple of basis points on the MBS beyond the buydown cost. Loans with a full-term interest-only structure are also saving on the MBS due to strong market demand. With Treasuries seemingly range-bound at current levels, this should position Fannie and Freddie for continued tightening into year-end.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.