- Market volatility surrounding tariff announcements caused significant spread widening in early April

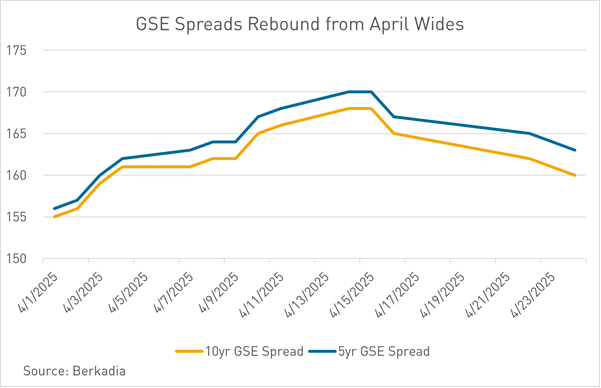

- Agency CMBS spreads have found their footing in the market, driven by solid investor demand

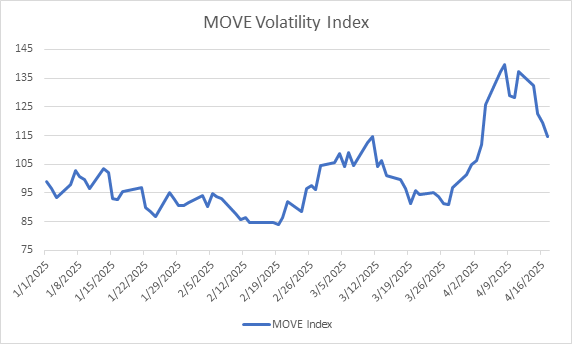

- Treasury volatility continues to plague the market due to general fiscal & monetary policy uncertainty

Agency CMBS spreads have found stability in the market following early April widening. Strong demand for Agency CMBS paper has driven spreads to tighten ~5bps across tenors this week and deals with full-term interest only structures are trading even tighter. Supply of new issue Agency CMBS has been light over the past two weeks, averaging less than half the $1.5 billion weekly run rate we’ve been experiencing recently. This dip in supply, which has likely been exacerbated by treasury rate volatility, has helped drive spreads tighter. Deals that utilize a rate buydown continue to get the best execution in the market due to their convexity profile, driving strong investor demand.

*Source: Berkadia

Agency CMBS spreads widened significantly in early April following President Trump’s ‘Liberation Day’ tariff announcement, and the general market turmoil that ensued. The widening was caused by a number of factors, including the general market volatility caused by the uncertainty surrounding fiscal policy moving forward. The MOVE index, which tracks bond market volatility, spiked in early April. In times of general uncertainty investors tend to be more risk-adverse, lightening demand for Agency CMBS and driving spreads wider. General market volatility caused dramatic swings in treasury rates, which dipped during the early days of the tariff announcements. This dip in treasury rates caused a surge in originations which was met by weak market demand, putting further upward pressure on spreads. Finally, there was a significant swing in the SWAPS market caused by an unwinding in basis trade. This volatility in the SWAPS market caused further pain on Agency CMBS spreads, as investors scrambled to price deals appropriately. MBS levels widened nearly 15bps across tenors in early April, but have since tightened 5bps off of these YTD highs.

*Source: Bloomberg LP

GNMA project loan and construction loan spreads have also found stability following significant widening in early April. An avalanche of new origination in early April caused more significant widening on GNMA spreads than on Agency CMBS – over $500mm in new origination hit the street in a week, drastically higher than the typical $100-200mm. Spreads widened 30bps in early April, but since found their footing. The modeling & pricing of GNMA securities relies heavily on future rate projections – spreads should find further stability when clarity arises on future fiscal & monetary policy.

Volatility caused by the tariff announcement rippled throughout the CRE financing universe, not just Agency CMBS – bridge lenders have increased their pricing since April 1st, with most indicating an addition of 25 to 50 basis points to their spreads. For example, a lender previously offering S+225-250 is now quoting S+275-300. However, the higher cost debt fund lender have not moved as much, still pricing around S+500. The CMBS market has also slowed down in recent weeks – according to Commercial Mortgage Alert issuers stepped cautiously back into the CMBS market this week, with spreads tightening in some cases. While spreads remained well wide of where they started the month, two conduit offerings and a single-borrower deal were making the round with investors.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.