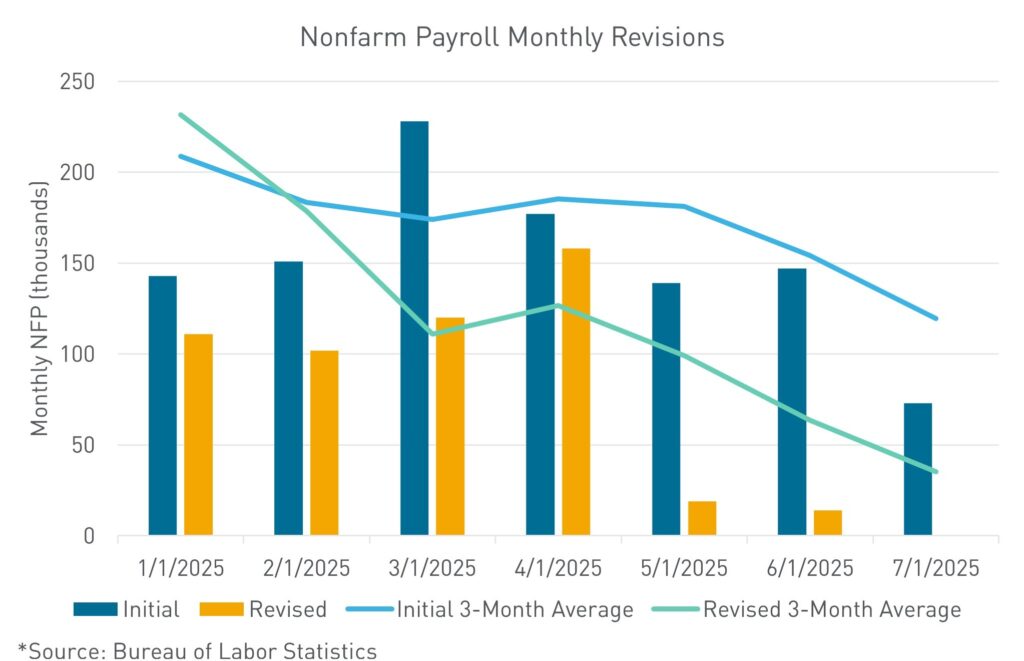

- July payrolls disappoint; revisions reveal a dramatically weaker labor market

- Tariff-driven inflation persists, but consumer spending remains flat

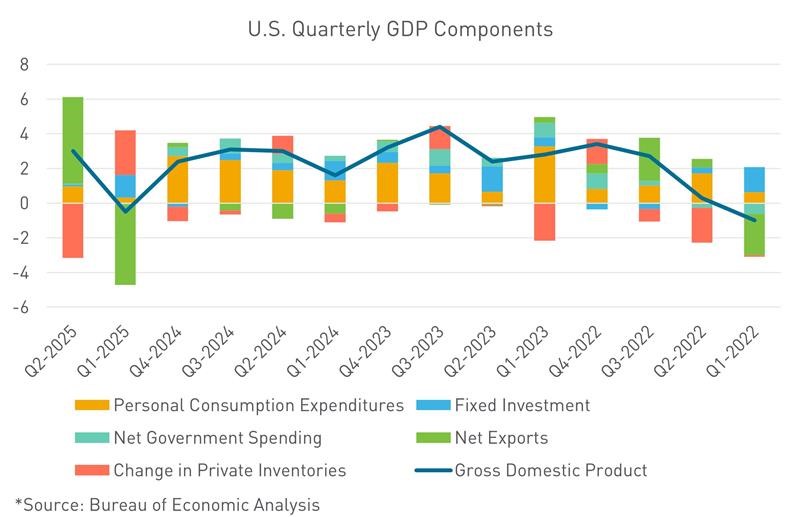

- GDP Print more anomaly than trend

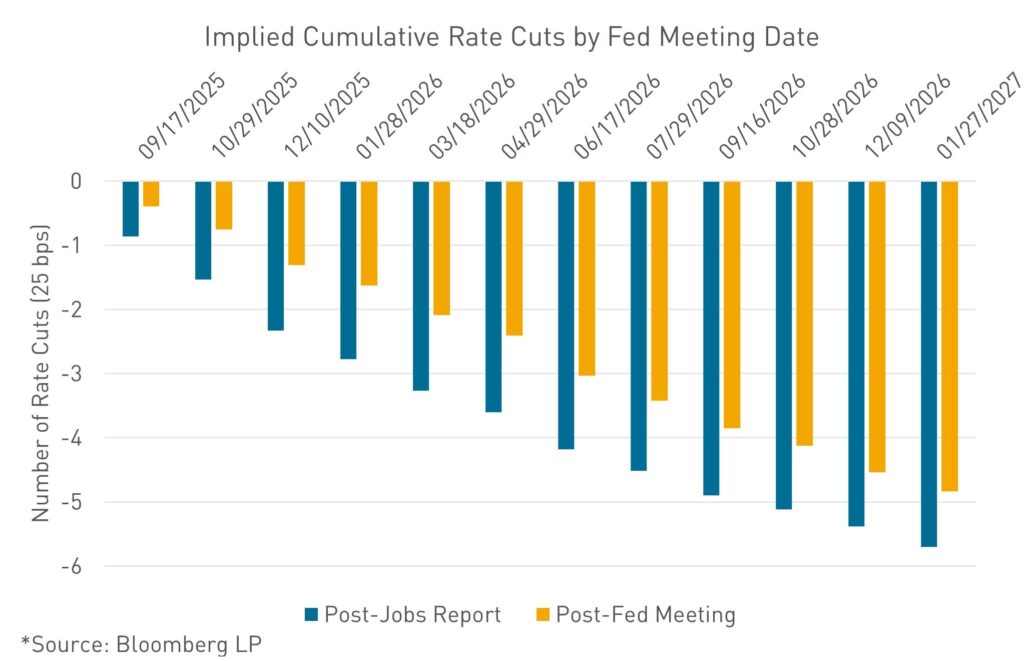

- Rate cut expectations recalibrated amid shifting economic signals

In the span of two days, the macro market feels like it has been turned upside down. On Wednesday, the Federal Open Market Committee (FOMC) voted to hold its benchmark rate steady at 4.25%–4.50% during the July meeting. Notably, Fed Governors Waller and Bowman dissented, advocating for a rate cut—the first dual dissent since 1993. The Fed’s statement acknowledged that “growth of economic activity moderated in the first half of the year,” while maintaining that “labor market conditions remain solid” and inflation “remains somewhat elevated.” Markets were largely unmoved, as the decision aligned with expectations.

The July jobs report, released Friday morning, has dramatically reframed the labor market narrative. Employers added just 73,000 jobs in July, well below expectations. More strikingly, revisions to May and June payrolls slashed previously reported gains by 258,000 jobs. This recalibration shifts the three-month average for job creation from 150,000 to just 35,000—a stark contrast that suggests the labor market may be weaker than previously understood.

This new data challenges the Fed’s assertion that the labor market is “broadly in balance.” While Powell cited quits, job openings, and the unemployment rate to justify a solid labor market, the revised payroll figures tell a different story. The unemployment rate ticked up to 4.2%, and hiring has slowed across most sectors, with gains concentrated in healthcare and social assistance.

At the press conference, Fed Chair Jerome Powell set a hawkish tone—Powell stated that a wide set of indicators suggest that conditions in the labor market are broadly in balance and consistent with maximum employment. After the labor market prints today, the two dissenters—while still likely political in their objection—do feel more vindicated. Powell’s hawkish stance at the press conference caused future projections to wane. In the days before the FOMC meeting, the market projected a 68% chance of a September rate cut, dropping to 39% after his press conference, only to rally back to an almost 90% chance after Nonfarm Payrolls Friday morning.

While the headline Q2 GDP growth of 3.0% initially appeared strong, a closer look reveals a far more unstable economic foundation. The bulk of the growth was driven by a surge in net exports, largely the result of front-loaded shipments ahead of anticipated tariff changes—a temporary distortion rather than a sign of sustainable demand. Final sales to domestic purchasers increased by only 1.1%, and consumption grew at a modest 1.4%, with notable weakness in services and housing. These figures suggest that underlying demand is softening, and with labor market cracks now emerging, the economy may be more vulnerable than the top-line numbers suggest.

The July jobs report has exposed cracks in the labor market, with payroll revisions painting a dramatically weaker picture than previously accepted. The collapse in the three-month average job gains signals a sharp loss of momentum and raises concerns about underlying labor market fragility. While Powell maintained a hawkish tone earlier in the week, the data now suggests that the Fed may soon face a more urgent trade-off. If the unemployment rate continues to rise meaningfully from its current 4.2%, the Fed will likely be compelled to cut rates—even if inflation remains above target—as preserving labor market stability becomes the dominant priority.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.