- August Nonfarm Payrolls print missed expectations to the downside while unemployment ticked up

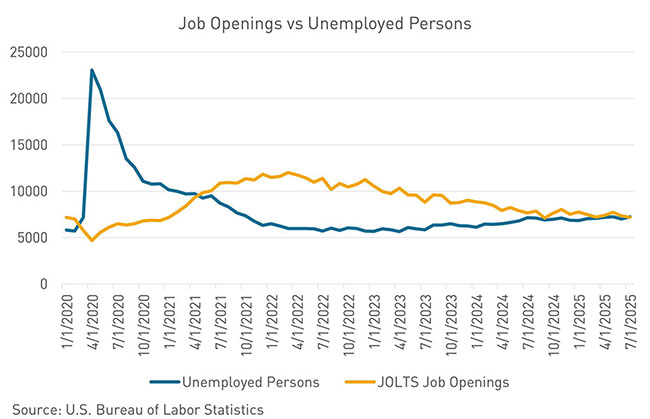

- July JOLTS figure shows that unemployed persons outnumbered job openings for the first time this cycle

- Traders pencil in a rate cut at the September FOMC meeting

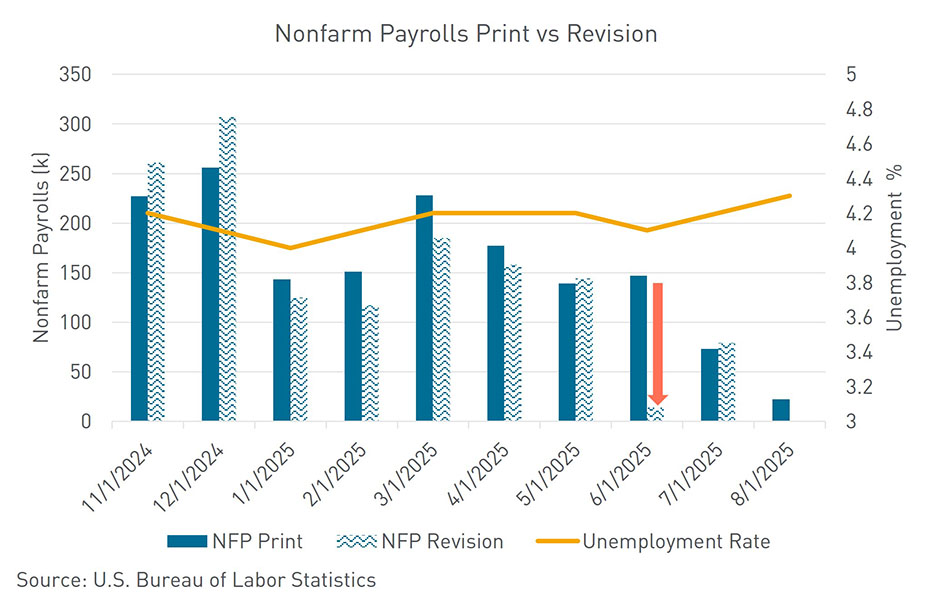

The FOMC has had ample time and data between the July and subsequent September meetings to study the U.S. macroeconomic landscape – the consistent theme of a weakening labor market has paved the way for the Fed to resume rate cuts, despite a murky picture on inflation. The July Nonfarm Payrolls print missed expectations to the downside, and the previous month’s data was revised lower so significantly that President Trump fired the commissioner of the Bureau of Labor Statistics. At the Jackson Hole Symposium, following the July NFP print and downward revision, Fed Chair Jerome Powell hinted that the Fed may resume cutting rates should the labor market continue to deteriorate. The August Nonfarm Payrolls and Unemployment figures, released on Friday morning, proved this theme consistent.

Nonfarm Payrolls increased 22,000 in August, according to the Bureau of Labor Statistics report, significantly below market expectations of 75,000. The unemployment rate ticked up to 4.3%, tying the highest levels seen in the current economic cycle. While July payrolls were revised slightly higher, the jobs picture looked even worse in June. The adjustments follow the sizable downward revisions seen in the last jobs report, which were the largest since 2020. Accounting for the revisions in this report, employment growth in the last three months has averaged just 29,000. Payrolls have come in under 100,000 for four straight months, extending the weakest stretch of job growth since the pandemic. June was revised downward by 27,000 from +14,000 to -13,000, and July was revised upward by 6,000, from +73,000 to +79,000.

Economists have characterized the labor market as a low-hiring, low-firing environment, though layoffs are picking up. Job growth was concentrated in health care and leisure and hospitality – job growth in private education and health was up 47,000, while leisure and hospitality had a 28,000 increase. Despite the growth in health care and social assistance, the increase was the smallest monthly increase since January 2022. The impact of policies of the Department of Government Efficiency are still playing out – federal government employment fell by 15,000 in August (-15,000) and is now down by 97,000 since January.

The July JOLTS report, released on Wednesday, provided further evidence of a weakening labor market. U.S. job openings fell in July to the lowest in 10 months, with available positions decreasing to 7.18 million from 7.36 million in June. The pullback in openings was driven by health care, retail trade, and leisure and hospitality, with vacancies in health care dropping to the lowest level since 2021. The slide in vacancies indicates companies are becoming more cautious and selective with their hiring as they attempt to gauge the impact of President Donald Trump’s trade policy on the economy. In addition to the openings data, the pace of hiring has slowed, and it is taking longer for unemployed people to find another position.

Notably, the number of job openings per unemployed worker decreased to 1:1, hovering at the lowest level since 2021. At its peak in 2022, the ratio was 2:1. This ratio is watched closely by Fed officials as a proxy of the balance between labor supply and demand. The 1:1 ratio provides evidence that any ongoing inflationary price pressures are not being caused by the labor market.

The deteriorating labor market data has given the Fed the green light to begin cutting rates at the September meeting; however, the number of rate cuts following September remains in flux. The odds of a third rate cut in 2025 increased significantly this week as traders prepared for a dramatic shift in monetary policy. The 10-year UST is down nearly 20bps since the Labor Day holiday.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.