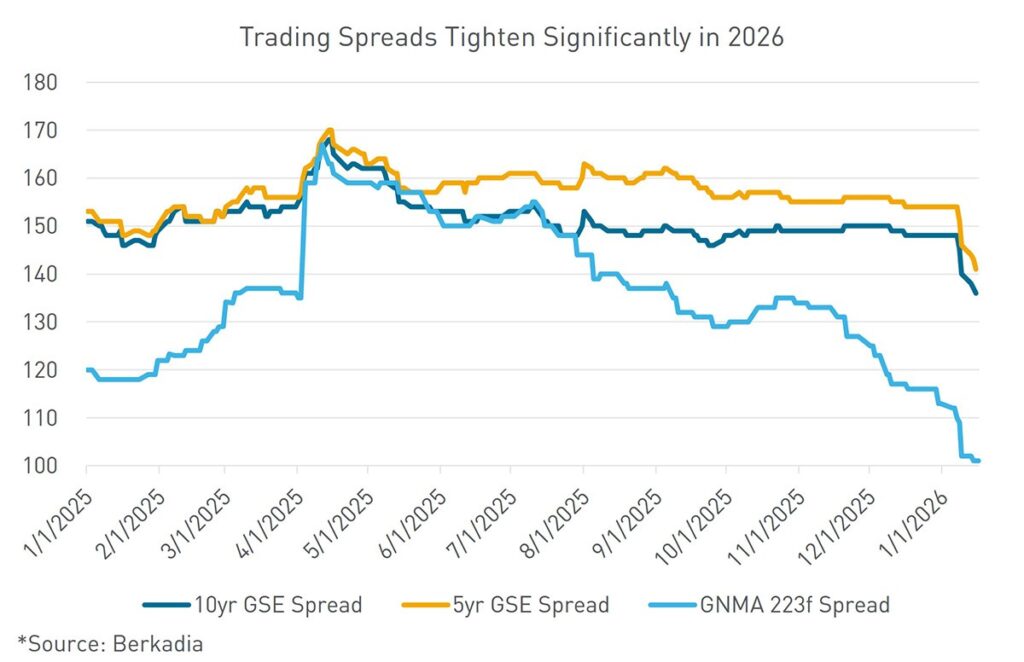

- Agency CMBS tighten significantly to start the year following Trump tweet

- Macroeconomic prints resume following government shutdown

- Political pressures increase on Fed Chair Powell

Commercial real estate capital markets, particularly in the multifamily space, are taking the “new year, new me” mantra very seriously. Liquidity is bountiful in the space; trading spreads have tightened significantly; and a regime change is on the horizon at the Federal Reserve. The Federal Housing Finance Agency (FHFA) increased agency multifamily loan purchase caps to $88 billion per agency, up 20.5% from 2025. The continued 50% mission-driven business requirement and exemption for workforce housing loans support strong financing availability for affordable housing. Aside from the Agencies, third-party lending sources are also eager to put capital to work, with life companies, debt funds, and banks all gearing up for a banner year.

Agency Commercial Mortgage-Backed Securities (CMBS) trading spreads are also starting the year on an optimistic note. On Thursday, January 8, President Trump announced in a tweet that he is directing his representatives at the government-sponsored enterprises (GSEs) to purchase $200 billion in mortgage-backed securities (MBS), a move he said is intended to bring mortgage rates down. The announcement has had a direct impact on Agency CMBS spreads—Fannie Mae Delegated Underwriting and Servicing (FNMA DUS) spreads are approximately 15 bps tighter in January across tenors. Trading volumes have been sparce despite the spread-tightening, with under $650 million of new issuance volume since the announcement, half the volume seen in a typical week in 2025. A slow start to the year was expected, with issuers and buyers off their desks while attending the Commercial Real Estate Finance Council (CREFC) conference. In December, Fannie Mae made a policy change to allow a full 2% buydown on 5-year and 7-year tenor deals—subject to certain credit restrictions—mirroring the Freddie Mac position. The policy change should continue to drive volumes of the shorter-term tenors, as spreads with a full 2% buydown look extremely attractive.

Ginnie Mae 223f spreads have also tightened significantly to start the year and currently sit at their tightest levels since May of 2022. Broker-dealer demand for the product began to ramp up in the third quarter of 2025, partially driven by the steepening of the yield curve. Volume was curbed in the fourth quarter due to a pause in the release of firm commitments during the government shutdown—the combination of low volume with increased dealer demand helped drive spreads tighter. Ginnie Mae (GNMA) spreads have tightened further to start the year, despite volume picking up, riding the tailwinds of the Trump tweet.

The Fed enters the year with question marks surrounding future policy. After cutting rates by 25 bps at the December Federal Open Market Committee (FOMC) meeting, overnight rates are now 175 bps lower than the peak of the cycle. Fed Chair Jerome Powell stated in the December press conference that Fed funds are now “within a range of plausible estimates of neutral and leave us well-positioned to determine the extent and timing of additional adjustments” to rates. The Fed’s dot plot, on the other hand, portrays a notably wide grouping of rate projections for 2026, illustrating that FOMC voting members generally lack consensus surrounding the neutral rate.

Of the three FOMC members who dissented at the December meeting, two cited inflation concerns as their reason for favoring steady rates. At the time, key inflation data was unavailable due to the government shutdown. Since then, Consumer Price Index (CPI) releases have resumed and are coming in at a more subdued pace. If inflation readings continue to drift toward the Fed’s 2% target, policymakers may feel more confident that tariff-related policies will not reignite price pressures. Chair Powell continues to face political scrutiny as his term draws to a close, underscoring the importance of Federal Reserve independence at a time when markets are navigating both technological transition and geopolitical uncertainty.

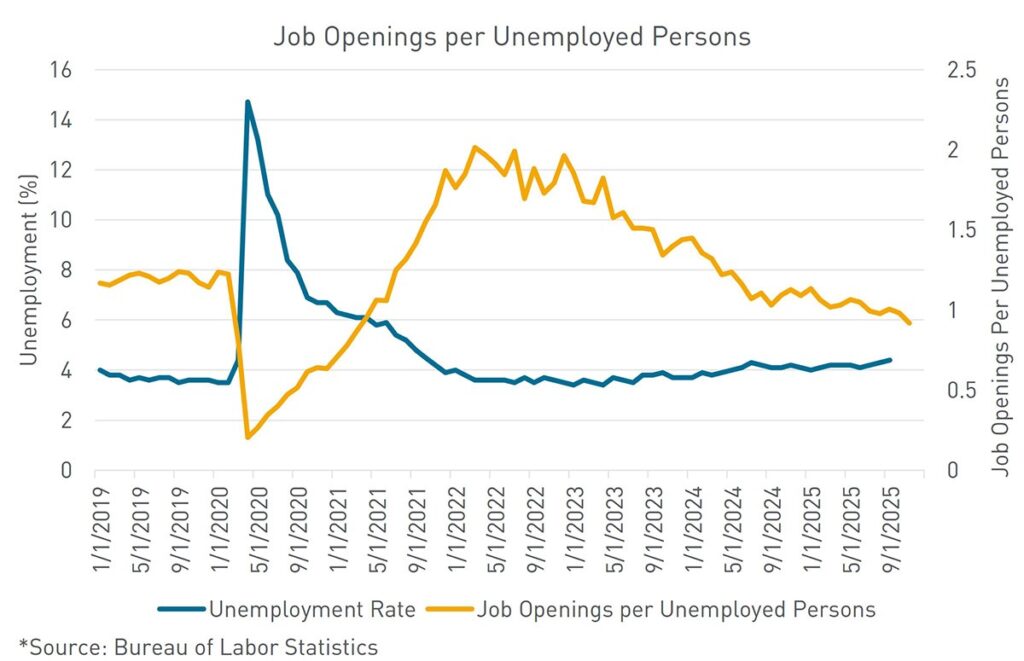

The primary argument for continued rate cuts now rests with the labor market. Nonfarm payroll growth remains soft, with several recent revisions turning negative. Although the shutdown left officials without government labor data in December, private sector indicators helped fill the gaps. Recent Job Openings and Labor Turnover Survey (JOLTS)-style data from private providers show the ratio of job openings to unemployed workers falling below 1:1—a level Fed officials watch closely as a gauge slack in the labor market. A ratio at or below parity suggests the labor market is no longer a source of inflationary pressure. For markets, the interplay between easing inflation and weakening employment data, as well as a to-be-named Powell successor, will define expectations for the Fed’s next moves.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.