- U.S. engagement with Iran ignites inflation fears due to projected increase in oil prices

- Market volatility spikes with the duration of the conflict unclear

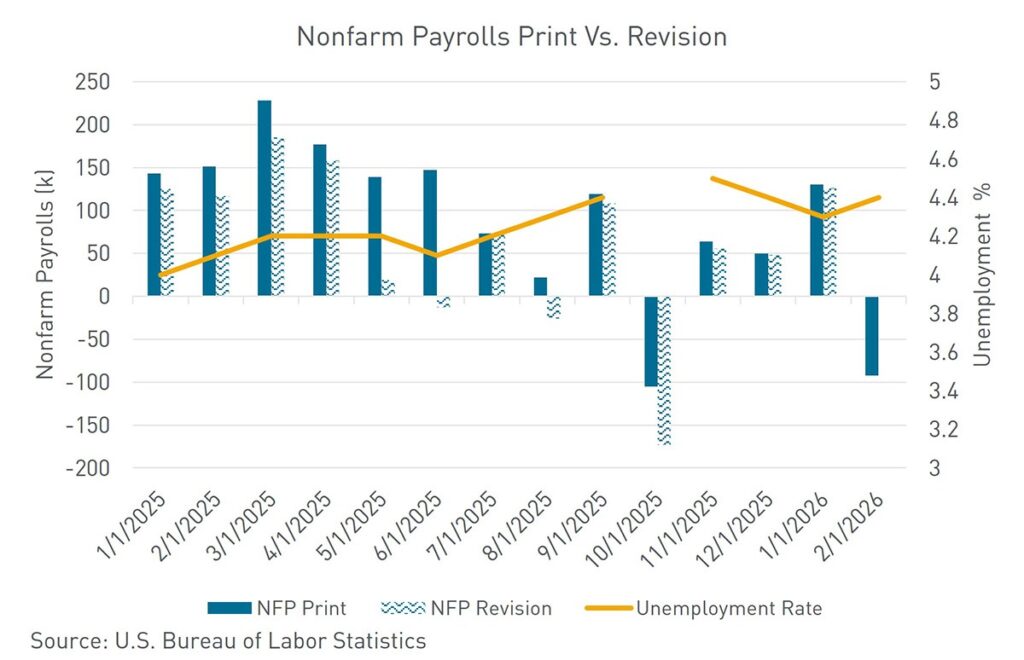

- February nonfarm payroll print misses significantly to the downside

The Federal Reserve is in desperate need of a timeout. Just five weeks ago, the Federal Open Market Committee (FOMC) was content with the state of the U.S. economy. Fed officials believed current rates were at appropriate levels to promote progress on the Fed’s dual mandate. Jerome Powell was running out the clock on his term as Chair, stating at the January FOMC meeting that current rates were in a plausible range of neutral. Since the January meeting, however, the script on the U.S. economy has been flipped. What looked like a controlled endgame just weeks ago now feels more like a sudden momentum swing. Investors will have to wait until the March 18 FOMC meeting to receive some direction; until then, policymakers will remain sidelined as markets move faster than expected.

The Fed’s dual mandate—to promote maximum employment and stable prices—typically functions like a seesaw. When one side weakens, the FOMC can deploy monetary policy to boost the underperforming objective while placing pressure on the other. Recent economic prints show a schism in the seesaw, raising serious concerns for the U.S. economy.

On the inflation side, price pressures are re-emerging. Heightened geopolitical tensions with Iran have raised concerns about higher energy prices, while Personal Consumption Expenditures (PCE) and Producer Price Index (PPI) prints came in hotter than expected, driven primarily by continued strength in services inflation. Adding to the uncertainty, the Supreme Court’s ruling invalidating President Trump’s prior tariff policies—followed by the administration’s temporary tariff response—has further clouded the inflation outlook.

At the same time, the labor market is also showing significant signs of weakness. The Bureau of Labor Statistics reported on Friday that the U.S. lost 92,000 jobs in February, and the unemployment rate increased to 4.4%. The Fed’s traditional playbook—supporting one half of the dual mandate at the expense of the other—will be put to the test, as both employment and price stability appear to be moving in the wrong direction.

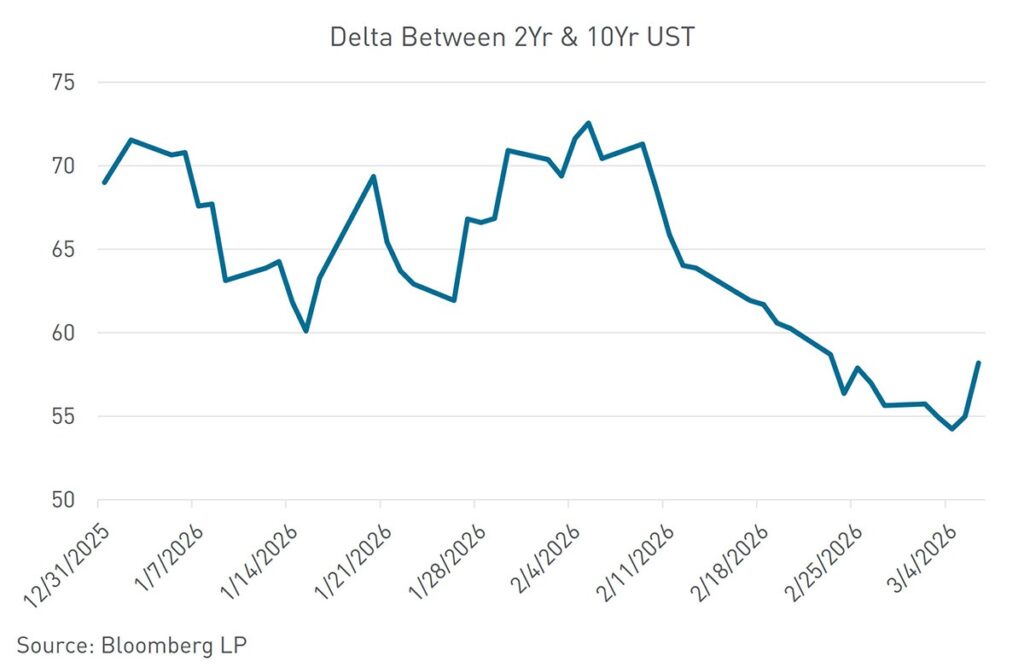

In prior periods of market stress, U.S. Treasuries reliably served as a “flight to safety” destination—capital flowed in, and yields moved lower. Today’s backdrop is more complicated. The initial reaction to the data was a Treasury selloff, with yields moving higher, but the move reversed midday as Treasuries rallied and yields were sent lower across the curve, reflecting a shift as investors reassessed what the data implied for growth and the Fed’s path. The widening on the 2s–10s U.S. Treasury yield curve underscores concerns about the growth outlook rather than inflation alone.

The curve’s behavior captured that tug of war. Longer dated yields, which had initially tracked renewed inflation anxieties tied to higher oil prices and Middle East tensions, ultimately followed the broader rally as the market shifted from “inflation shock” back to “growth scare.” Meanwhile the front end—most sensitive to near-term Fed expectations—remained anchored by the idea that weakening labor and consumer momentum increases the odds that the Fed leans towards support rather than restraint. In other words, the day’s tape wasn’t a clean flight-to-quality bid, nor a straightforward inflation-led selloff—it was a live repricing of which risk dominates: structurally higher inflation or deteriorating growth. That uncertainty, more than any single data point, is what’s complicating the traditional Treasury playbook.

U.S. employers unexpectedly cut jobs in February, while the unemployment rate ticked higher, challenging the view that the labor market was stabilizing. Nonfarm payrolls declined by 92,000 last month—one of the largest monthly drops since the pandemic—following a strong start to the year. The data also highlights how heavily recent labor-market momentum has relied on a single sector: healthcare. More than 30,000 Kaiser Permanente employees were on strike for much of the month, creating a partly anticipated temporary drag, alongside weather-related impacts. Even so, job losses were broad-based, with declines spanning a wide range of industries.

Taken together, the data raise fresh questions about whether the labor market is truly steadying—as many Wall Street economists and Federal Reserve officials had expected—after the weakest year for hiring outside of a recession in decades.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.