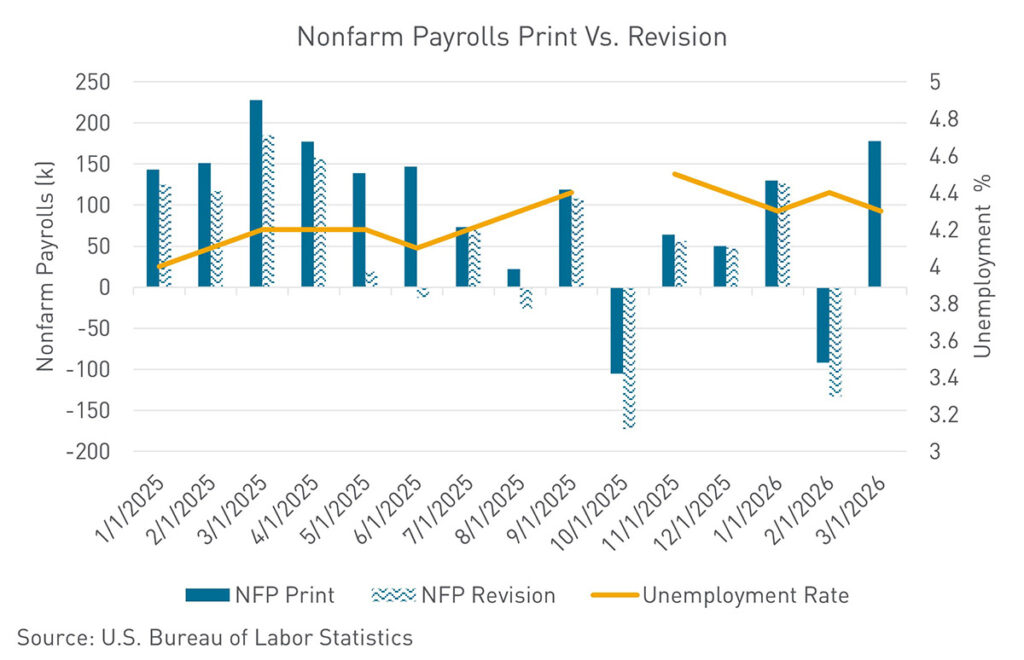

- March nonfarm payrolls rebounded sharply to 178,000, beating all estimates, with unemployment falling to 4.3%

- Powell signaled longer-term inflation expectations remain anchored, reinforcing the Fed’s wait-and-see posture

- Escalating energy disruptions tied to the conflict in Iran keep the inflationary backdrop fragile

The U.S. macroeconomic landscape has been generally off-kilter for over a month—this week, the economy received some much-needed clarity on both sides of the Fed’s dual mandate. This morning’s March nonfarm payrolls report delivered an unambiguous upside surprise, with job growth rebounding sharply, offering reassurance that the employment side of the Fed’s dual mandate remains intact. On the other side of the dual mandate, Fed Chair Jerome Powell signaled that the Fed believes longer-term inflation expectations remain anchored, even as energy prices surge. The path forward for monetary policy, however, continues to hinge on a variable outside the Fed’s control—the trajectory of oil markets, which continue to be roiled by the ongoing conflict in Iran.

The March nonfarm payrolls report, released Friday morning, delivered a meaningful upside surprise and offered evidence that the U.S. labor market remains on solid footing despite a rapidly shifting macroeconomic backdrop. Payrolls rose 178,000, the strongest monthly gain since late 2024 and above Bloomberg survey estimates—the print follows a sharper-than-published decline of 133,000 in February. The February figure, revised down from the initially reported -92,000, was distorted by a combination of a Kaiser Permanente health care worker strike affecting more than 30,000 employees in California and Hawaii, and severe winter weather. The unwinding of both factors drove much of March’s rebound, with healthcare, construction, and leisure and hospitality all recovering. The unemployment rate fell to 4.3% from 4.4%, and given rounding conventions, the underlying rate could plausibly have printed at 4.2%.

The three-month average for payroll employment now stands at approximately 68,000. The core theme of the current labor market is a no-hire, no-fire economy: businesses are neither aggressively expanding headcount nor initiating layoffs. For the Federal Reserve, that dynamic removes the urgency of cutting rates to defend the employment side of the dual mandate, while leaving the central bank free to remain focused on its more pressing concern: inflation.

Speaking at Harvard University on Monday, Fed Chair Jerome Powell offered the market a carefully calibrated message. Longer-term inflation expectations, he noted, appear to be well-anchored beyond the near term. Powell characterized the Fed’s current policy stance as content to wait and see, acknowledging that the economic effects of the ongoing conflict in Iran and the associated energy shock remain genuinely uncertain. He was careful to note that while officials may ultimately need to respond to the inflationary impact of higher oil prices, that moment has not yet arrived.

His framing on supply shocks was instructive. The Fed’s default tendency is to look through energy-driven price spikes, treating them as temporary disturbances rather than structural inflation. Powell acknowledged that instinct but made clear that it comes with an important qualifier: supply shocks still require careful monitoring of inflation expectations, which for now, appear contained.

The geopolitical backdrop continues to cast a long shadow over the U.S. macroeconomic outlook. West Texas Intermediate (WTI) crude settled above $110 a barrel for the first time since 2022 this past Thursday, and gasoline prices at the pump have surpassed $4 a gallon nationally, a level not seen in nearly four years. The closure of the Strait of Hormuz, through which roughly one fifth of the world’s oil and liquefied natural gas supplies ordinarily flow, has been the primary driver.

More than 40 allied nations convened virtually on Thursday to coordinate efforts to reopen the strait, with many making clear that planning for a pathway that does not depend on U.S. leadership may be necessary. The United Nations Security Council is expected to vote on a related resolution on Friday. The strait itself remains all but closed, with only a trickle of vessels managing to transit. Diesel prices in Europe have risen above $200 a barrel, and fuel costs are climbing across Asia and other nations globally.

From a monetary policy standpoint, the conflict in Iran remains the key wildcard. Powell’s message—that the Fed can hold steady as long as inflation expectations remain anchored—is a conditional one. Should energy prices continue to rise, or should inflation expectations begin to drift, the calculus changes. For now, today’s strong labor market data removes the pressure to cut rates, while Powell’s remarks have removed the immediate pressure to hike. The Fed is in a genuine holding pattern.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.