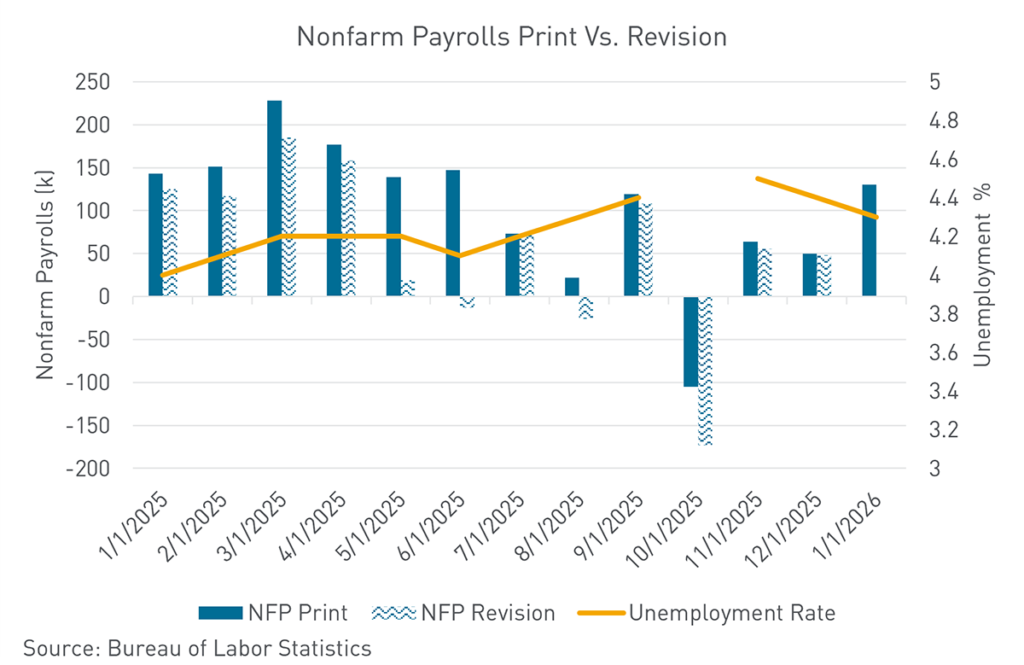

- January Nonfarm Payrolls beat expectations, driven by healthcare jobs

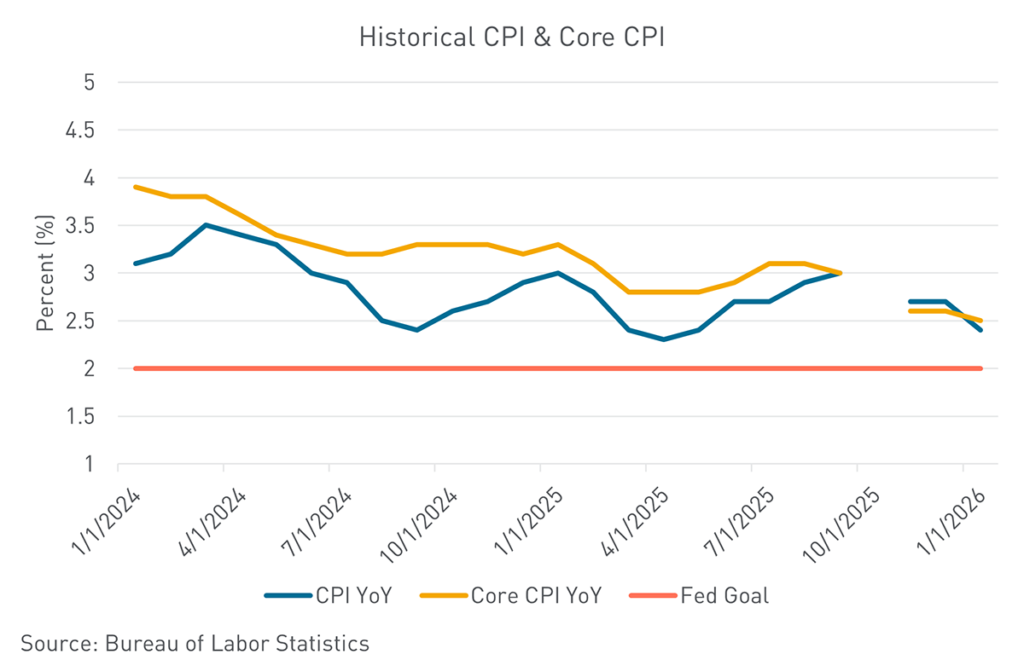

- January headline CPI cools, but core increases month over month

- Traders increase projections for a third rate cut in 2026

The job of the Federal Reserve is straightforward: keep the U.S. economy on solid footing with good growth. Through the Federal Open Market Committee, the Fed sets monetary policy with two goals in mind – maximum employment and stable prices – commonly known as its “dual mandate.” This week’s economic prints exhibited a dual mandate double feature of critical labor market and pricing indicators – Nonfarm Payrolls and Unemployment Rate were released on Wednesday, and the Consumer Price Index (CPI) figure was released on Friday.

On the employment front, January delivered the strongest payroll growth in more than six months, while the unemployment rate unexpectedly fell. Employers added 130,000 jobs and the unemployment rate declined to 4.3%, according to the Bureau of Labor Statistics. Job gains averaged just 15,000 a month in 2025, but the January nonfarm payrolls report suggests that the labor market may be finding footing after the slowest year for hiring outside of a recession since 2003. While economists generally expect hiring to remain slow in 2026, more clarity around the impact of President Trump’s economic policies and easing borrowing costs could encourage employers to increase headcount.

The pickup in January hiring was overwhelmingly driven by the health care sector, with nearly all the 130,000 new jobs tied to healthcare or related fields. Over the past year, demand for healthcare workers has effectively propped up the labor market as other sectors reined in hiring or even shed jobs. Construction and professional and business services also added jobs, while manufacturing recorded its first monthly gain in employment in more than a year. Federal government payrolls continued to decline. The narrow concentration of job growth to the healthcare sector may prove worrisome to FOMC members – the January print points to a largely stagnant labor market outside of healthcare.

Foreign-born workers are heavily concentrated at the upper and lower ends of the skill ladder in healthcare. In 2024, immigrants accounted for less than 15% of the U.S. population, but 39% of home health aides, 28% of physicians, and 24% of dentists, according to census data aggregated by IPUMS. Immigrant labor also plays a significant role in construction, where around one-quarter of workers are foreign-born, census data shows. That share rises sharply in certain construction specialties, with immigrants making up around half of all drywall installers and roofers, 45% of painters, and 39% of general laborers.

The second act of the dual mandate double feature was the January CPI report, which showed inflation cooling modestly at the headline level. Headline CPI increased by 0.2% month over month, down from December’s 0.3% reading. Core CPI, which excludes food and energy prices, moved in the opposite direction, increasing to 0.3% vs. 0.2% in December. The slight pickup in core inflation reflected higher prices for airline fares, personal care, recreation, medical care, and communication. Prices for used cars and trucks, household furnishings, and auto insurance decreased. One of the key drivers of post-pandemic inflation has been housing costs – shelter prices rose just 0.2% in January, the smallest gain since September.

January inflation readings have been elevated in recent years, often beating expectations as companies tend to raise their prices at the start of the year. Against that backdrop, Friday’s CPI report was a constructive signal, easing concerns that the Trump administration’s tariffs will lead to broader, sustained inflation pressures. Over the course of the week, traders increased projections for rate cuts in 2026 – Bloomberg’s WIRP function increased the projected 2026 rate cuts from 55bps on Monday to 65bps on Friday, implying growing odds of a third cut later in the year. With inflation fears generally curbed, market attention is likely to shift squarely back to the labor market in the months ahead.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.