- U.S. Government shutdown stalls the release of nonfarm payrolls and unemployment prints

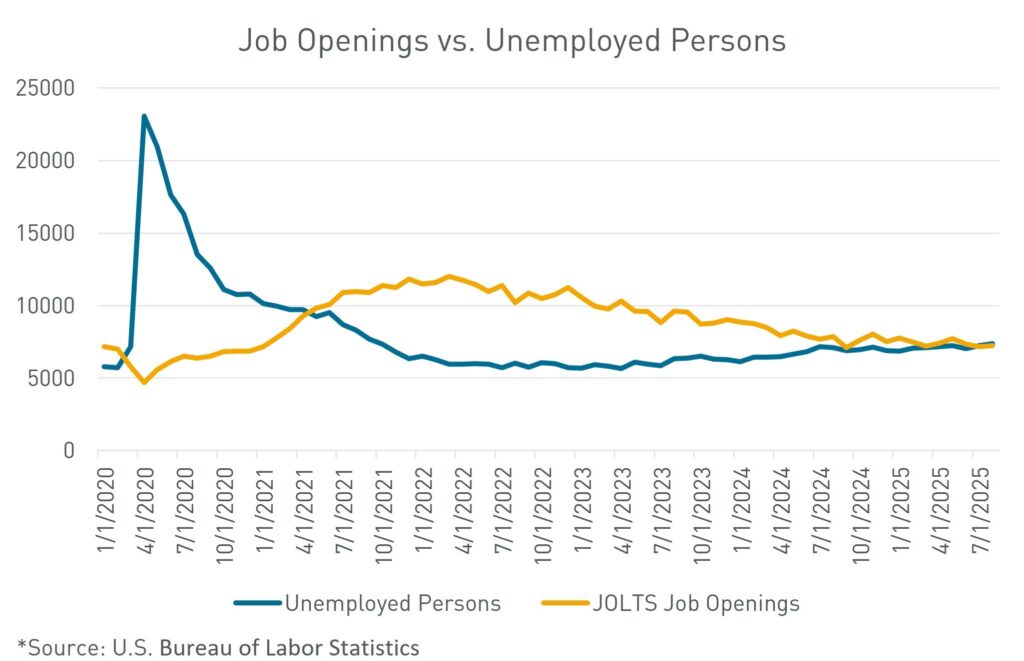

- August JOLTS details a further deteriorating labor market

- Agency CMBS spreads tighten through quarter-end

A headline week for the labor market turned into a nothingburger when the September Nonfarm Payrolls and Unemployment release was put on hold due to the government shutdown. The prints will be released upon the government’s reopening; however, the delay leaves the Federal Open Market Committee (FOMC) without pivotal data leading into their October meeting. The Fed restarted its rate-cutting campaign at the September meeting due to signs of a weakening labor market. Without the nonfarm payrolls and unemployment figures, committee officials will need to rely on other sources of data in order to make future monetary policy decisions. According to Bloomberg, the market is currently pricing in a 98% chance of a rate cut at the October FOMC meeting.

One data point on the labor market that the Fed can analyze before the next meeting is the Job Openings and Labor Turnover Survey (JOLTS) report. The U.S. JOLTS Report was released on September 30, before the government shutdown—job openings were little changed in August, while hiring was subdued, according to the Bureau of Labor Statistics. The hiring rate fell to 3.2%, the lowest since June 2024, while the number of people who voluntarily left their jobs dropped to the lowest level this year. The print highlights the continued theme of a weakening labor market, as the demand for workers remains weak. For the second straight month, the ratio of the number of job openings per unemployed worker decreased below 1:1. At its peak in 2022, the ratio was 2:1. This ratio is watched closely by Fed officials as a proxy of the balance between labor supply and demand. The sub-1:1 ratio provides evidence that any ongoing inflationary price pressures are not being caused by the labor market.

Agency Commercial Mortgage-Backed Securities (CMBS) spreads tightened throughout the month of September, indifferent to typical widening pressures seen at quarter-end. Short tenor spreads notably tightened more significantly than longer tenor spreads, reversing a trend of underperformance seen since late May. This year, the majority of new issuance Agency CMBS has been 5-year tenor. While this dynamic remains true, the tightening of 5-year spreads has been driven by an increase in investor demand for the paper. Ginnie Mae (GNMA) spreads also had an excellent month of September—223f spreads tightened by nearly 10 basis points over the course of the month. Investor demand has increased significantly for new-issue GNMA paper, partially driven by the steepening of the yield curve. Spreads tightened despite an atypically large volume of new issuance this month. The increase in volume was driven by the recent changes to Mortgage Insurance Premium (MIP) guidelines.

The release of the nonfarm payrolls and unemployment figures upon the reopening of the U.S. government will surely cause some general market volatility—the Agency CMBS market is vibrant, with able liquidity available to absorb any uptick in issuance.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.