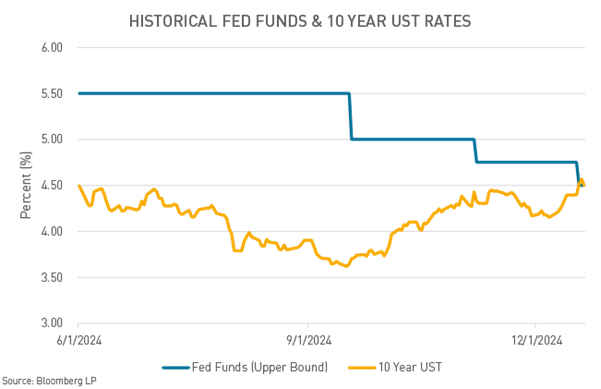

- The FOMC voted 11-1 to cut rates by 25 bps, lowering the target range to 4.25%-4.50%

- This marks the third consecutive cut, totaling 100 bps from the peak

- Updated projections show higher inflation, stronger GDP, and lower unemployment

- Fewer rate cuts are expected in 2025, with the Fed signaling a cautious approach moving forward

The Federal Open Market Committee (FOMC) concluded their final meeting of the year on Wednesday, where committee members voted 11-1 to cut rates by 25 basis points, lowering its target range to 4.25%-4.50%. The move marks the third consecutive rate cut from the Fed, reflecting a cumulative 100 bps of rate cuts from their 5.25%-5.50% peak. The Fed’s updated Summary of Economic Projections (SEP) revealed a hawkish shift, with just two rate cuts now expected in 2025, down from four. Recent inflation data, including rising Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) figures, has reversed earlier optimism, with core inflation still above the Fed’s 2% target. Labor market data, initially seen as weakening, has since rebounded. September and November job reports showed strong hiring, with Powell emphasizing that the labor market remains “solid” and not a significant driver of inflation.

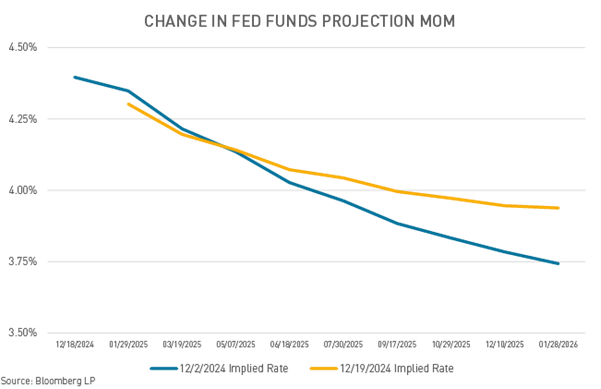

The Fed’s updated projections prompted markets to reprice expectations for future rate cuts and economic productivity. Earlier this month, Bloomberg’s WIRP function forecasted 61 bps of rate cuts in 2025, implying at least two cuts, but Wednesday’s meeting revealed a more hawkish outlook. Projections now show just one cut in July, with a second not expected until September 2026. This shift rippled through markets, triggering a selloff in 10-year Treasury rates, now over 40 bps higher than early-December lows. The Dow fell 2.6% during a 10-day losing streak (its longest losing streak in 50 years), while the S&P 500 and Nasdaq dropped 3% and 3.6%, respectively. The U.S. dollar also surged to a two-year high.

Why Cut Rates Now?

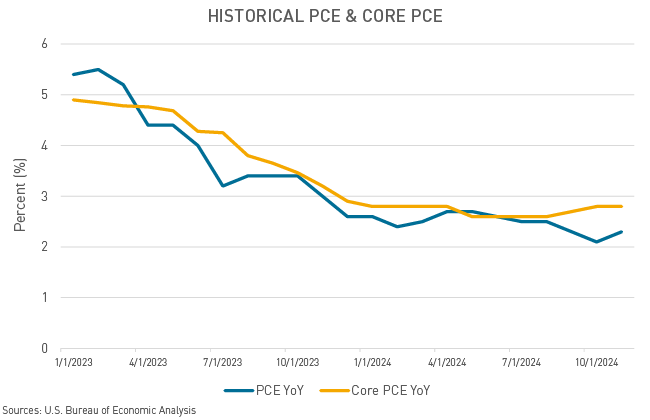

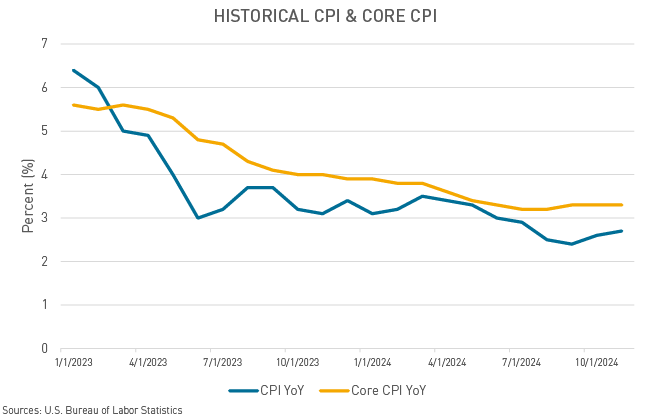

Despite stalling inflation and a resilient labor market, Powell defended the cut, arguing that it positions the Fed to respond flexibly to future data. He reiterated that rates remain restrictive while acknowledging inflation’s persistence. The Fed will continue seeking the “neutral rate” while maintaining flexibility under the incoming administration. “Today was a closer call, but we decided it was the right call,” Powell said at a news conference after the meeting. He later added, “From here, it’s a new phase, and we’re going to be cautious about further cuts.” November’s PCE inflation rose slightly, with year-over-year PCE at 2.4% (up from 2.3%) and Core PCE steady at 2.8%, both above the Fed’s 2% target. Core CPI also climbed, with November’s print marking the fastest monthly increase in 18 months, driven primarily by vehicle prices. Chair Powell reiterated that inflation remains the Fed’s primary focus, requiring further progress before additional rate cuts are considered.

But What About That Labor Market?

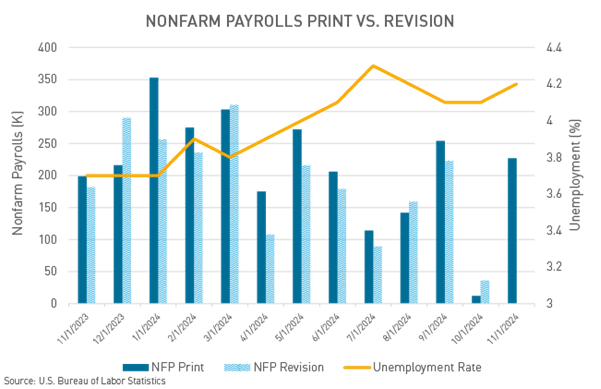

The September 50 bps cut, driven by fears of a weakening labor market, may have been an overreaction. Labor data has shown improvement since then. Unemployment has declined from July highs, and hiring has picked up. September’s Nonfarm Payrolls (NFP) report showed 254,000 jobs added, far exceeding the 150,000 forecast and marking the largest monthly gain since March. While October’s NFP was skewed by hurricane impacts, November’s report was strong, though unemployment ticked up slightly.

The December FOMC meeting highlighted the Fed’s ongoing struggle to balance inflationary pressures with a resilient labor market, all while maintaining flexibility in an uncertain economic and political environment. The 25-bps rate cut, coupled with a more hawkish outlook for 2025, signals a cautious pivot as the Fed seeks to recalibrate policy toward a neutral stance. With inflation still above target and labor market fears easing, the Fed’s path forward will depend heavily on incoming data, leaving markets to navigate an era of heightened uncertainty and recalibrated expectations – all key ingredients for heightened volatility.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.