- The Federal Open Market Committee (FOMC) voted 9-3 to cut its target benchmark rate by 25 basis points at its December meeting

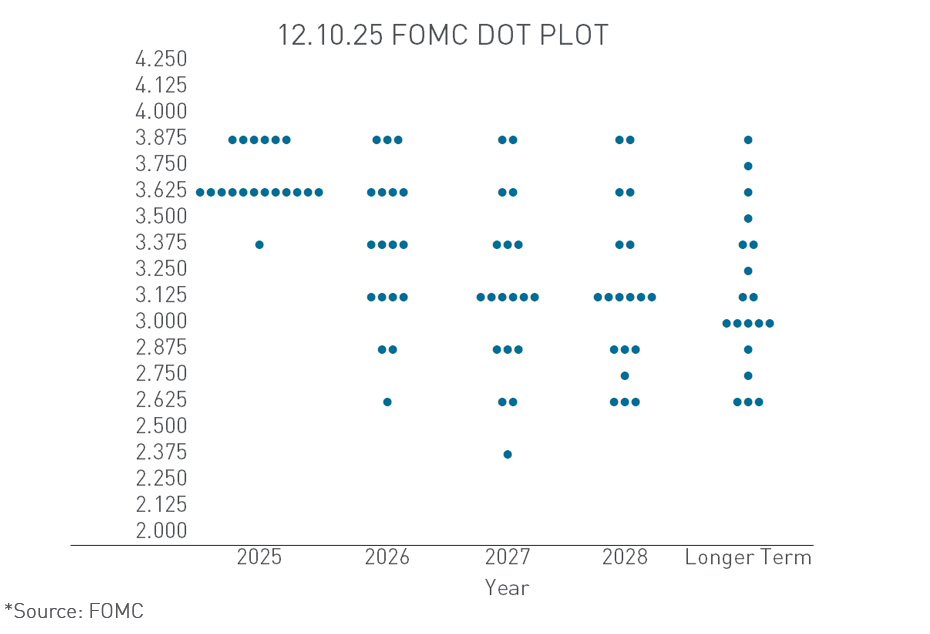

- The Fed’s refreshed Summary of Economic Projections decreased its forecast for inflation in 2026, increased its forecast GDP

- Fed Chair Powell stated that rates are now “within a range of plausible estimates of neutral”

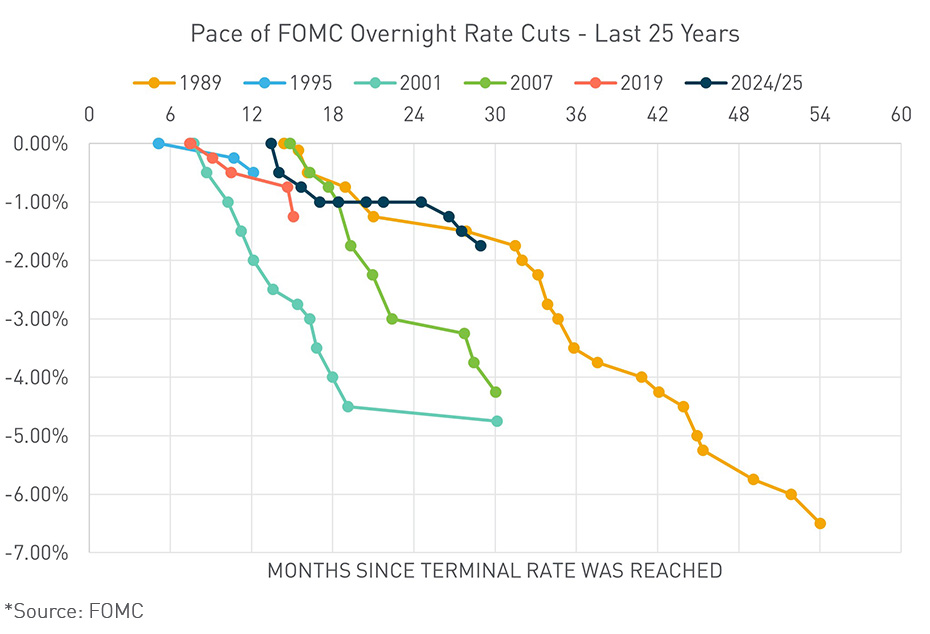

The Federal Reserve held its final meeting of the year on Wednesday. Committee members voted 9-3 to cut the benchmark rate by 25 basis points to a 3.50%–3.75% range. The move was the third consecutive rate cut from the Fed, and overnight rates are now 175 basis points lower than their peak of the cycle. Fed Chair Jerome Powell stated in the press conference that Fed funds are now “within a range of plausible estimates of neutral and leave us well-positioned to determine the extent and timing of additional adjustments” to rates. Powell doubled down on this notion later in the press conference, stating again that the Fed is now within a “broad range” of estimates of a neutral policy setting and will now await economic developments.

The Fed released its quarterly update of the Summary of Economic Projections (SEP). The “dot plot” rate projection shows the median official expected to lower rates by a quarter point in 2026 and another quarter point in 2027, the same as projected in September. The refreshed SEP projected an inflation rate of 2.4% by the end of 2026, down slightly from 2.6% forecast in September, and sees Gross Domestic Product (GDP) growth of 2.3%, compared with 1.8% previously.

Three committee members dissented from consensus—Schmid and Goolsbee voted for no rate change, while Miran voted for a 50 bp cut. Chicago Fed President Austan Goolsbee voted to dissent for the first time since he joined the central bank in January 2023. In an interview with CNBC, Goolsbee said that he is projecting more interest rate cuts than many of his colleagues but dissented against a rate cut this week because he wanted to wait for more data on inflation.

Powell addressed the dissenting votes numerous times in the press conference. When asked if the broader sense of dissent among Fed presidents raises the bar for further rate cuts, Powell said the backdrop here is that there are risks both to inflation and to the job market, and differences of view turn on where the bigger risk is seen, but discussions are thoughtful and respectful. Powell said he doesn’t think that the Fed is at a point where dissents are unproductive, noting that he could himself make a case for either side of the policy argument.

The drought of recent economic data, caused by the government shutdown, helped drive the lack of consensus amongst committee members. Powell said that available data show that the outlook for employment and inflation has not changed much since the last meeting, and highlighted that the weak labor market is due to slower labor force growth, paired with a lower demand for workers. Powell stated, “There is no risk-free path for policy as we navigate this tension between our employment and inflation goals.” While general consensus is for the Fed to pause its rate-cutting campaign, projections could quickly change should the labor market continue to weaken.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.