- FOMC members voted 10-2 to cut rates by 25 bps, lowering the target range to 3.75%–4.00%.

- Fed Chair Jerome Powell hawkishly faded market projections for a December rate cut.

- The Fed announced that they will stop Quantitative Tightening via balance sheet runoff on December 1.

Fed Chair Jerome Powell was feeling festive on Wednesday when he spooked the market, hawkishly fading the notion that a rate cut at the December Federal Open Market Committee (FOMC) meeting was a guarantee. Powell’s sentiment reflected continued division amongst committee members—instead of playing down the fractured committee, Powell leaned into it, highlighting general uncertainty in monetary policy moving forward.

The FOMC voted 10-2 to cut its target benchmark rate by 25 basis points to a 3.75%–4.00% range at the October FOMC meeting on Wednesday. Two committee members dissented from consensus. Stephen Miran voted for a 50 bp cut, while Kansas City Governor Jeff Schmid voted for no rate change. In addition to the Schmid dissent, four of 12 regional bank presidents submitted a request for no change in the discount rate, sometimes seen as a form of soft dissent. These developments suggest the Committee may need to see some more evidence of a weakening jobs market before agreeing to another cut. The Fed’s statement maintained its prior description of the labor market, noting that “job gains have slowed, and the unemployment rate has edged up but remained low through August,” adding, “More recent indicators are consistent with these developments,” and “downside risks to employment rose in recent months.”

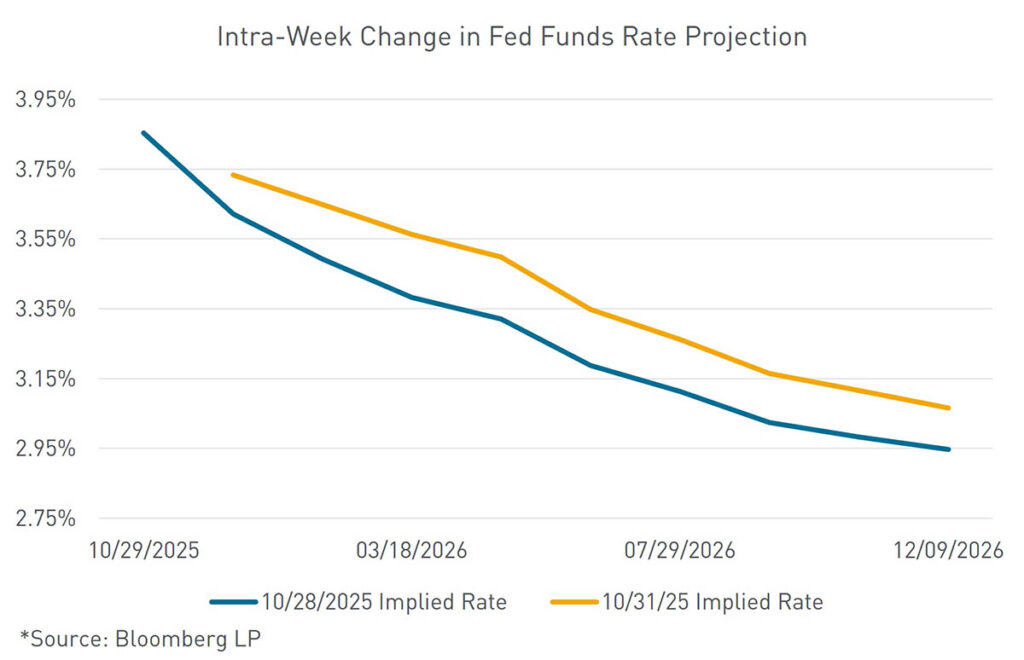

The sentiment of a divided committee was reflected heavily in Powell’s press conference. Powell opened the door for optionality moving forward by stating that a rate cut at the December FOMC meeting is “far from” a foregone conclusion. Powell’s hawkish hedge for a December rate cut may reflect the Fed’s lack of confidence/feel for the real-time economy, given the absence of labor market and inflation readings during the government shutdown. “There were strongly differing views today, and the takeaway from that is that we haven’t made a decision about December, and we’re going to be looking at the data that we have, how that affects the outlook and the balance of risks,” Powell said. On Tuesday, the market was projecting a 93% chance of a 25 bp rate cut at the December Fed meeting. Following the press conference, market projections have fallen to a 62% chance of a cut. The 10-year treasury rate rose 10 bps intraday on Wednesday as a result of these shifting probabilities.

The FOMC announced that they will stop their balance sheet runoff, also known as Quantitative Tightening (QT), on December 1. The decision to stop QT was made following the runoff of over $2 trillion in treasuries and mortgage-backed securities (MBS) from the Fed’s balance sheet. Given recent pressure and volatility in overnight funding markets, the end of the Fed’s asset runoff was widely expected at this meeting or in December. Balance sheet runoff will continue in November, before the Fed enters “net neutral” on December 1. MBS runoff will continue at the current pace and be used to fund T-bill purchases, while coupon Treasury runoff will be reinvested in full at auction. “This takes some of the hawkish fears around reinvestment policy shifts off the table, just ahead of next week’s quarterly refunding,” Bloomberg Intelligence’s Will Hoffman said.

Inadvertently or not, the October FOMC meeting flipped the script on President Trump, putting pressure on the administration to reopen the government. The lack of economic data, put on pause due to the government shutdown, is causing general uncertainty amongst FOMC members on the health of the economy. When asked whether a prolonged government shutdown hinders the committee’s ability to make the right policy decision, Powell said, “We’re not going to be able to have the detailed feel of things.” Uncertainty regarding the possibility of a December rate cut will continue until the government eventually reopens. After all, according to the Fed Chair, “If you’re driving in the fog, you slow down.”

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.