U.S. ECONOMIC MACRO COMMENTARY & INSIGHTS

- FOMC cuts rates for the first time in over four years

- Committee members vote 11 to one to lower benchmark rate by 50 basis points to target range of 4.75%–5.00%

- The labor market will remain in focus for the foreseeable future

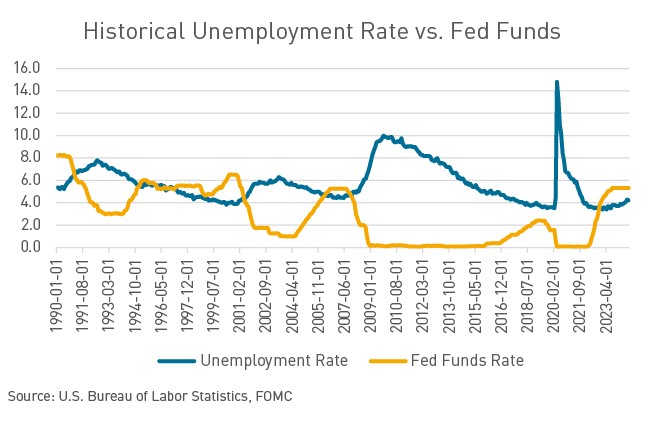

The long-awaited rate cut is finally here. On Wednesday the Federal Open Market Committee (FOMC) voted to lower interest rates by 50 basis points, the first rate cut in over four years. Wednesday’s decision marks a hard pivot in monetary policy as the Fed shifts focus from the price stability / inflation side of its dual mandate to the labor market side. “This decision reflects our growing confidence that with an appropriate recalibration of our policy stance, strength in the labor market can be maintained in a context of moderate growth and inflation moving sustainably down to 2%,” Fed Chair Jerome Powell said at Wednesday’s press conference. The Fed practiced patience in their battle against inflation, holding rates at the 5.25%–5.50% terminal rate range for nearly 14 months before pivoting in policy.

The 50 bp rate cut was a surprise to some market participants, especially with the presidential election on the horizon. While a rate cut never appeared to be in doubt this week, the size of the cut certainly was. The 50 bp cut suggests that the Fed is worried about the labor market, and recent prints have given them reason to be. The Nonfarm Payrolls and Unemployment, the Job Openings and Labor Turnover Survey (JOLTS) job openings, and ADP employment prints released in late August all missed analyst projections to the downside. On top of recent missed prints, the labor market reported that the U.S. economy created 818,000 fewer jobs than originally reported in the 12-month period through March 2024. Fed officials updated their quarterly economic forecasts on Wednesday, raising their median projection for unemployment at the end of 2024 to 4.4% from 4.0% forecast in June. The year-end unemployment rate forecast for next year is also 4.4%, same as the median Fed policymaker forecast for this year. While that could incorporate a higher peak rate at some point during 2025, it does suggest that the Fed expects the job market to remain strong, averting any big jump in unemployment. The Fed will be keeping a keen eye on the labor market; historically when the labor market weakens, the unemployment rises can spike quickly.

The Fed’s two-year battle against inflation seems to have finally come to an end. In their statement Wednesday, policymakers indicated that they now see the risks to employment and inflation as “roughly balanced.” The most recent Consumer Price Index (CPI) print was 2.5% with a Core CPI level at 3.2%, and the most recent Personal Consumption Expenditures (PCE) print was 2.5% with a Core PCE level at 2.6%. Recent prints have given FOMC members confidence that inflation will continue to trend towards the Fed’s 2% goal. The updated Summary of Economic Projections detailed a decrease in expected PCE level, the Fed’s preferred inflation gauge versus June forecasts. Committee members now project a 2.3% PCE level at the end of 2024, 2.1% to end 2025, and 2.0% to end 2026. In June, projections were 2.6%, 2.3%, and 2.0%, respectively. Recent inflation prints are convenient for the Fed, as it can take swift action against the weakening labor market with minimal fears of reigniting inflationary pricing pressures.

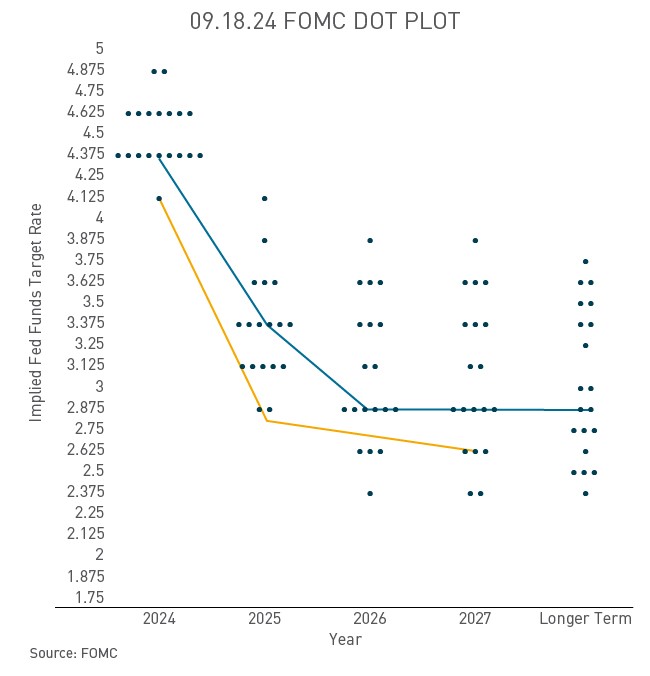

Fed Chair Powell led Wednesday’s press conference by proclaiming that the Fed is growing confident that with an appropriate recalibration of policy stance, strength in the labor market can be maintained, but the job market is not imparting inflationary pressure on the economy. “We are not on any preset course and will make our decisions meeting to meeting,” and “We will move as fast or as slow as we think is appropriate,” Powell said. The Fed’s dot plot shows the median expectation of 100 basis points of total cuts this year, implying two more quarter-point cuts or one larger half-point cut. Nine of the 19 officials penciled in 75 basis point of cuts or less, showing the margin here is thin. The median rate forecast for 2025 falls to 3.4% from 4.1% in June, implying four additional quarter-point moves next year.

The Fed has begun its search for the economy’s “neutral rate,” the interest rate that supports the economy at full employment / maximum output while keeping inflation constant. The Fed’s dot plot and the market’s projections disagree on the amount of rate cuts the Fed will need to achieve this theoretical level. The Fed will continue to leverage labor market prints to determine future policy, and market projections surrounding these prints will surely cause short-term treasury rate volatility. Trying to reconcile the Fed Chair’s press conference statements of “I don’t see anything in the economy right now that suggests the likelihood of a recession,” and that the committee is not in a rush to get to neutral (with the surprising jumbo cut) will keep the market off balance in future meetings but will likely further fuel the market belief that they can will another 50 bp cut into existence come November.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.