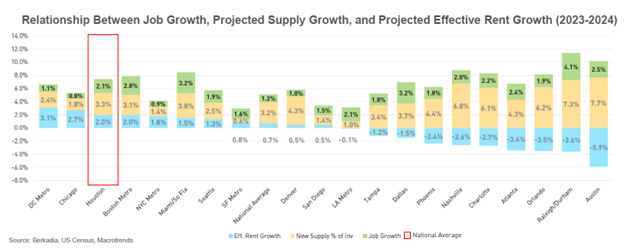

While the Houston MSA has consistently ranked among the top 10 markets for sales volume in the U.S., it has traditionally been overshadowed by neighboring markets such as Austin and Dallas. However, this year has been different – the Houston MSA is seeing an influx in private and institutional capital, and the macro-economic headwinds that had damped investment activity over the last few years, such as high interest rates, taxes, and insurance costs, have lessened. At the same time, the Houston job market is growing and projected supply for 2025 and 2026 is the lowest in the state on a percentage basis.

With investors identifying Houston as a “buy” market, the MSA stands out amid other active markets in Texas and is positioned incredibly favorably for 2025 and 2026.

Declining Interest Rates Drive the “Buy” Market

While high interest rates have persisted since early 2022, causing a fair amount of volatility, we’ve finally begun to see rates decline, instilling greater confidence from investors looking to enter the market.

Recent bidding activity following the first interest rate reduction in four years illustrates the growing confidence of buyers with increased participation and cap rate compression. Tour activity and buyer engagement has jumped across the board, but well-located assets available at a discount to replacement cost and new construction or turnkey assets in suburban areas with limited new supply, have drawn the most buyer attention in the latter half of 2024.

While more investors are now willing to participate in the market than there were in 2023, some sellers are still awaiting further rate decreases to transact, which we anticipate in Q4 and 2025. Once volatility adjusts, more sellers will be comfortable coming to market and transaction activity will continue to increase.

Insurance and Tax Concerns Lessen

Over the past several years, underwriting challenges associated with taxes and insurance have brought hurdles for CRE, specifically in the Sunbelt region. With assessed property values at a high, buyers had held off on investment activity.

However, we’ve seen decreases in assessed values in 2024, providing a much-needed relief to the valuation of these assets. It’s our belief that 2025 assessed values should be flat to down, as 2024 trades have provided more comps to the assessor’s office.

In the past few years, severe weather events have caused insurance rates to rise for property owners across the region. While grappling with evolving insurance policies can be challenging, insurance costs have stabilized or declined as we have progressed further into 2024. This has in turn boosted the value of assets, a trend that will continue into Q4 and 2025.

Strong Market Fundamentals Emphasize Multifamily Resiliency

From July 2023 through August 2024, Houston employers added 80,500 net new jobs that equated to a 2.4% total employment increase and ranked third in the U.S. In terms of both overall job gains and growth percentage, Houston outpaced both Dallas-Fort Worth and Austin, displaying strong employment trends that have continued to act as a driver for investor interest in the Houston MSA.

Consistent job growth has kept demand for rental housing high in the city with 14,000 units absorbed year to date and 17,000 absorbed over the last 12 months – both numbers above the 10-year average. Strong net absorption has accelerated rent growth in Houston, which has remained positive this year and has outperformed all its peers in Texas, which have substantially higher construction pipelines in terms of percentage of overall supply. CoStar is projecting that rent growth in Houston will average 3.4% annually from 2025 to 2027, nearly double the 1.8% average recorded in the five-year span before the pandemic.

In addition to strong employment trends and market fundamentals, the Houston MSA continues to attract new private capital to the market and is increasing its profile with institutional capital. With more investors ready to get off the sidelines and participate in transactions, deals are seeing a substantial uptick in the number of tours, offers from interested buyers, and more competitive terms in efforts to win deals.

Headwinds are Dying Down and All Signs Point to Houston

The Houston MSA has proven time and time again that it is one of the strongest multifamily markets in the US. This year especially, its operating fundamentals, influx of active capital, and the improvement seen in challenges associated with interest rates, taxes, and insurance, cement it as a stand-out market, making us incredibly optimistic for the remainder of the year and 2025.

– Berkadia Houston