- April CPI print rattled the market as oil prices continue to climb

- Traders increasingly question whether the Federal Reserve will be able to ease monetary policy at all this year

- Treasury rates continue to climb, curbing Agency CMBS volumes

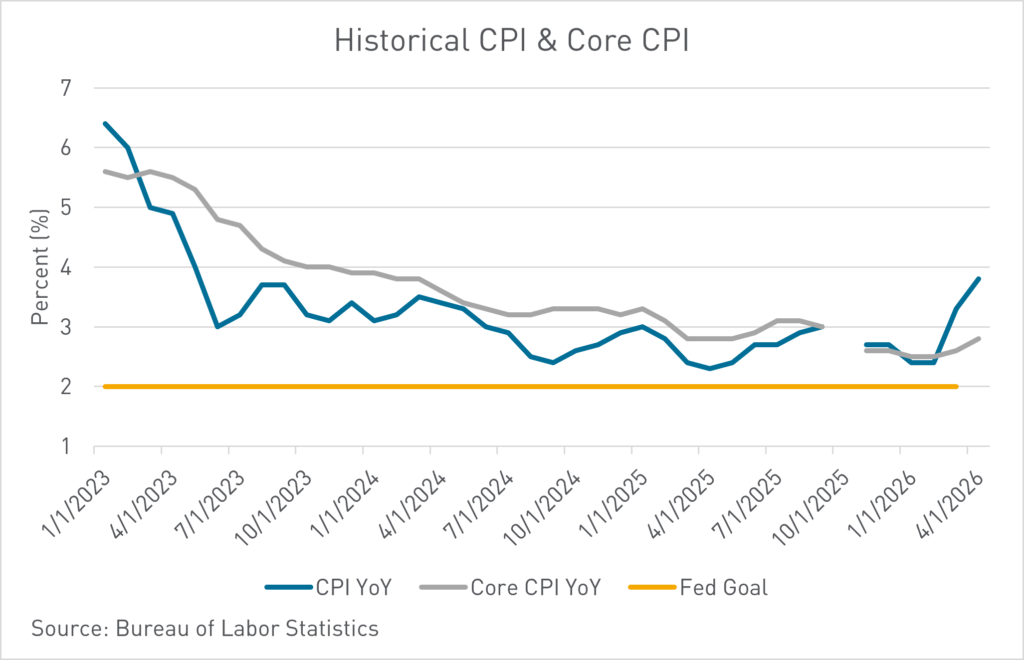

For a steady three years, besides a blip surrounding the Liberation Day tariff announcements, markets operated under the assumption that inflation was steadily moving back toward the Federal Reserve’s 2% target. April’s Consumer Price Index (CPI) report was the second straight data point that challenged the narrative. Consumer prices rose 3.8% year-over-year, above consensus expectations and marking the highest inflation reading since 2023. The acceleration was predominately driven by energy markets, and the broader market reaction suggested investors are becoming increasingly concerned that inflation pressures may no longer be confined to a temporary geopolitical shock.

The inflation surge was heavily tied to the ongoing disruption in global energy markets following the conflict involving Iran and the continued instability surrounding the Strait of Hormuz. Gasoline prices rose sharply throughout April as oil markets priced in prolonged supply disruptions and the possibility that commercial traffic through the Persian Gulf could remain constrained for longer than initially expected. Energy prices alone accounted for a substantial portion of the monthly increase in consumer prices, with gasoline prices rising more than 28% year-over-year.

*Source: Bureau of Labor Statistics

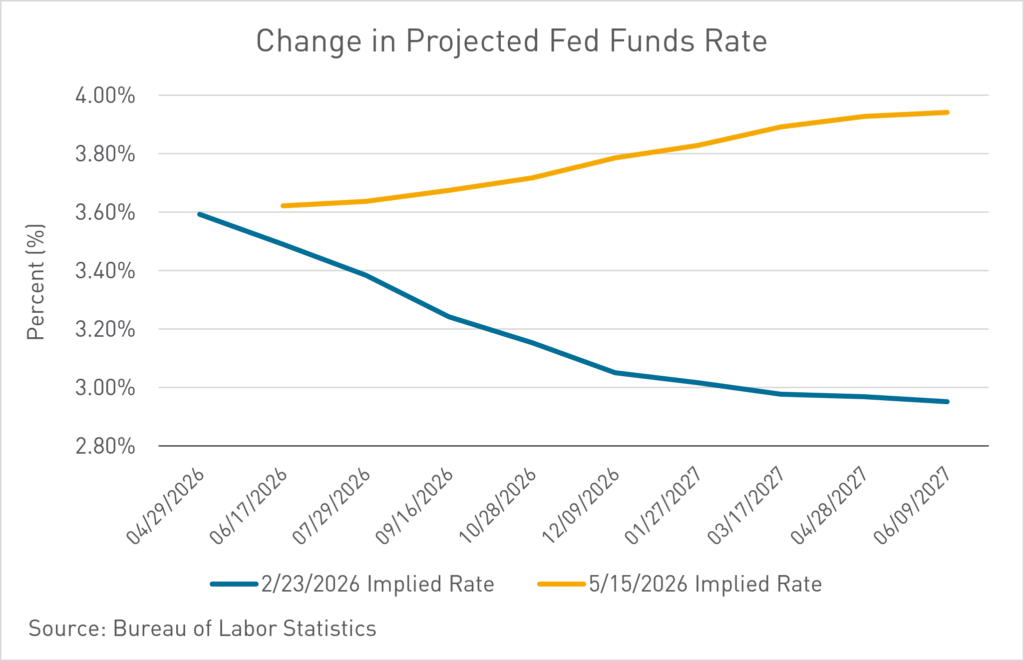

Treasury yields moved sharply higher across the curve immediately following the release, as investors increasingly questioned whether the Federal Reserve would be able to ease monetary policy at all this year. The concern is not simply that energy prices are temporarily higher, but markets are beginning to fear a broader second-round inflation dynamic. Higher fuel costs feed into transportation, logistics, manufacturing, aviation, and eventually consumer expectations themselves. The shift in psychology increasingly appears visible within bond markets. Longer-duration Treasury yields have continued climbing even beyond the immediate CPI reaction, reflecting a growing term premium and rising uncertainty surrounding long-run inflation stability. Investors are demanding greater compensation to hold long-dated government debt amid concerns that structurally higher deficits, geopolitical fragmentation, elevated commodity volatility, and deglobalization pressures could keep inflation above pre-pandemic norms for years to come.

*Source: Bloomberg LP

The latest inflation data highlights how fragile the post-pandemic disinflation process may ultimately prove to be. Prior to the Iran conflict, inflation had shown meaningful improvement, particularly in housing and core services. The recent energy shock demonstrates how quickly geopolitical disruptions can destabilize that progress. Inflation is no longer simply a domestic demand story—it has increasingly become tied to global supply chains, commodity markets, fiscal dynamics, and geopolitical risk.

All of this ultimately comes back to rates – and the path forward looks less anchored than it has in years. Markets are reconciling a more complicated policy backdrop: a transition in Fed leadership, a Fed that’s going to move with data, and a sticky inflation profile that may not glide back to target. The yield curve is beginning to reflect that uncertainty, with the front end repricing fewer cuts while the intermediate 5-10 year sectors reflects the higher-for-longer regime. The risk of delayed cuts – or even renewed tightening – keeps term premium elevated and borrowing costs stubbornly high across key CRE borrowing terms. In that environment, rates run the risk of becoming a structural constraint on capital formation, transaction speed, and overall market liquidity.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.