U.S. ECONOMIC MACRO COMMENTARY & INSIGHTS

- FOMC holds rates steady at July meeting

- The Fed has made significant progress on inflation; focus shifts to the labor market

- Market prices in at least one rate cut at September meeting

The Federal Open Market Committee (FOMC) members unanimously voted to hold rates steady at the July meeting. For an eighth straight meeting, the FOMC’s statement repeats language stating that the committee doesn’t expect to cut rates “until it has gained greater confidence that inflation is moving sustainably toward 2%.” The announcement and press conference certainly held a dovish tone, noting the significant progress made on inflation and the slight weakening seen in the labor market. Fed officials tweaked language in their statement to say that price pressures remain “somewhat” elevated and acknowledged “some further progress” towards their inflation goal, updated from “modest further progress” language in the previous statement. The statement notes that risks to achieving employment and inflation goals “continue to move into better balance.”

In his press conference, Fed Chair Jerome Powell noted that the Fed has made considerable progress on both sides of the Fed’s dual mandate: Inflation is significantly below cycle highs, and the labor market has come more into balance. Powell compared the current labor market to 2019, when the U.S. was not in an inflationary economy. “So, with the job market now back to similar conditions to then, labor dynamics aren’t likely to pose an inflationary impulse,” Powell said. He also said, “I would not like to see material further cooling in the labor market.”

Current monetary policy seems to echo the sentiment of Kenny Roger’s “The Gambler.” The FOMC is cautious of declaring victory on inflation prematurely, and in attempting to balance both sides of the Fed’s dual mandate, Powell said the Fed is preoccupied with balancing “the risk of going too soon versus too late.” (You’ve got to know when to hold ‘em, know when to fold ‘em.) Powell’s dilemma: “Go too soon and you undermine progress on inflation, wait too long and you put at risk the recovery.”

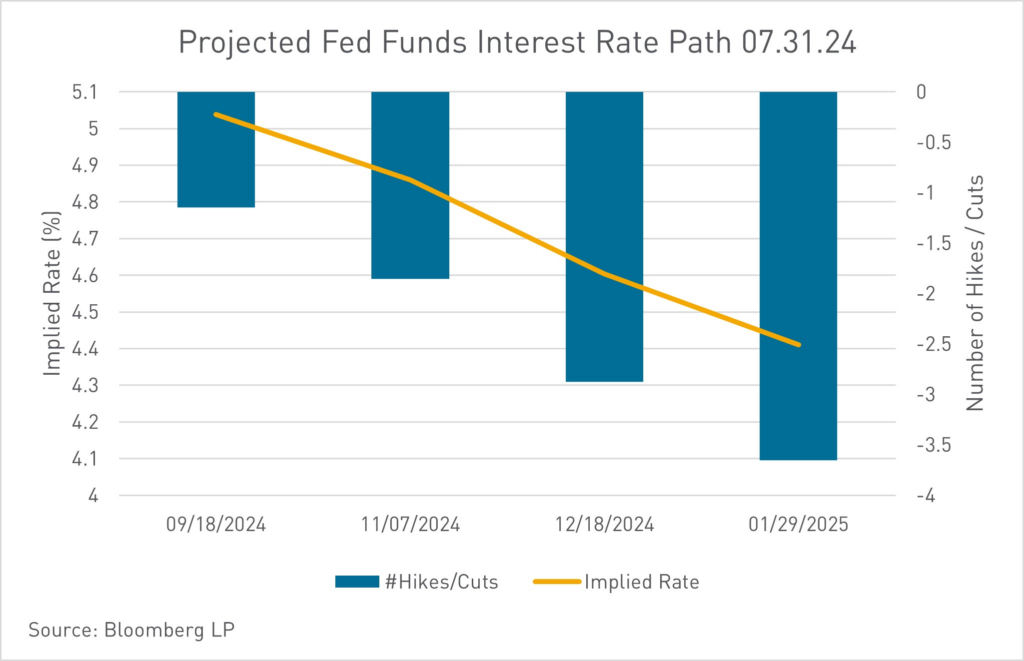

Market participants are interpreting the Fed’s announcement—plus recent inflation and labor market prints—with enough conviction to project a full rate cut at the September meeting. A total of 72 bps (nearly three full rate cuts) are currently projected before the end of the year, according to Bloomberg. Powell hinted towards the possibility of a September rate cut at his Wednesday press conference, saying, “a reduction in the policy rate could be on the table as soon as the next meeting in September. We’re getting closer to the point at which it’ll be appropriate to reduce our policy rate, but we’re not quite at that point.” Prior to the September FOMC meeting, all eyes will look towards upcoming labor market and inflation prints, as well as Powell’s remarks at the Jackson Hole Symposium, for future guidance.

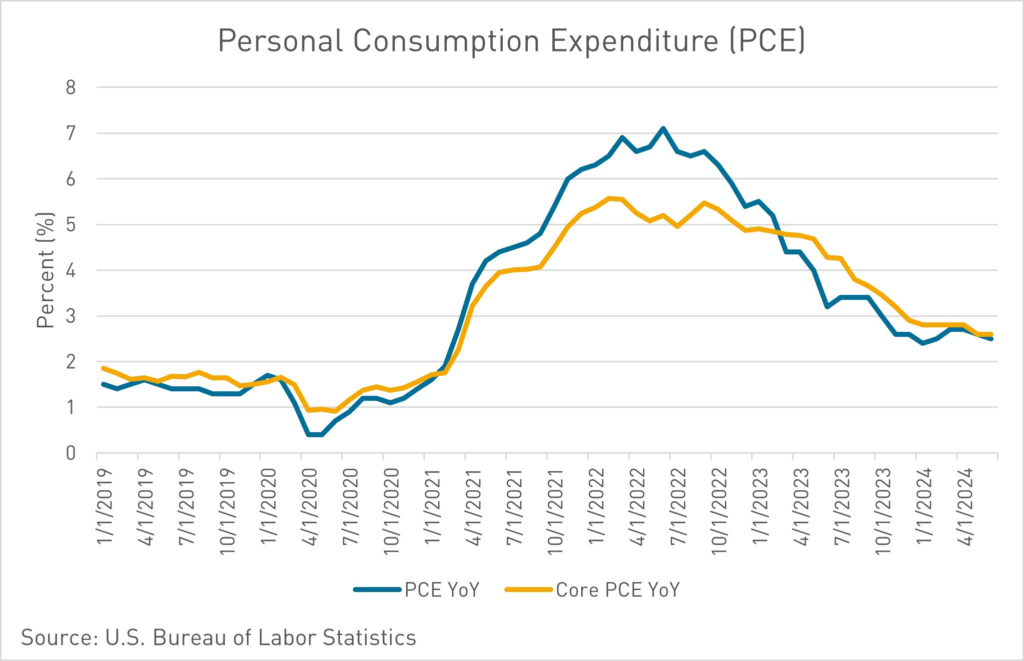

The July FOMC meeting was held a week after the June Personal Consumption Expenditures (PCE) price index print was released. PCE is known as the Fed’s preferred inflation gauge, and the June figures were particularly encouraging to the market. PCE was at 2.5% year over year, and the Core PCE level was 2.6%, significantly down from cycle highs and closing in on the Fed’s 2% goal. The Fed has two more inflation and jobs reports to consider before the September meeting. “The job is not done on inflation. Nonetheless, we can afford to begin to dial back the restriction in the policy rate,” Powell said. “You would think, in the base case, that policy rates would move down from here. I don’t want to try to give specific, you know, forward guidance about when that might be, the pace at which it might happen. That’s really going to depend on the economy. That’s highly uncertain.”

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.