U.S. ECONOMIC MACRO COMMENTARY & INSIGHTS

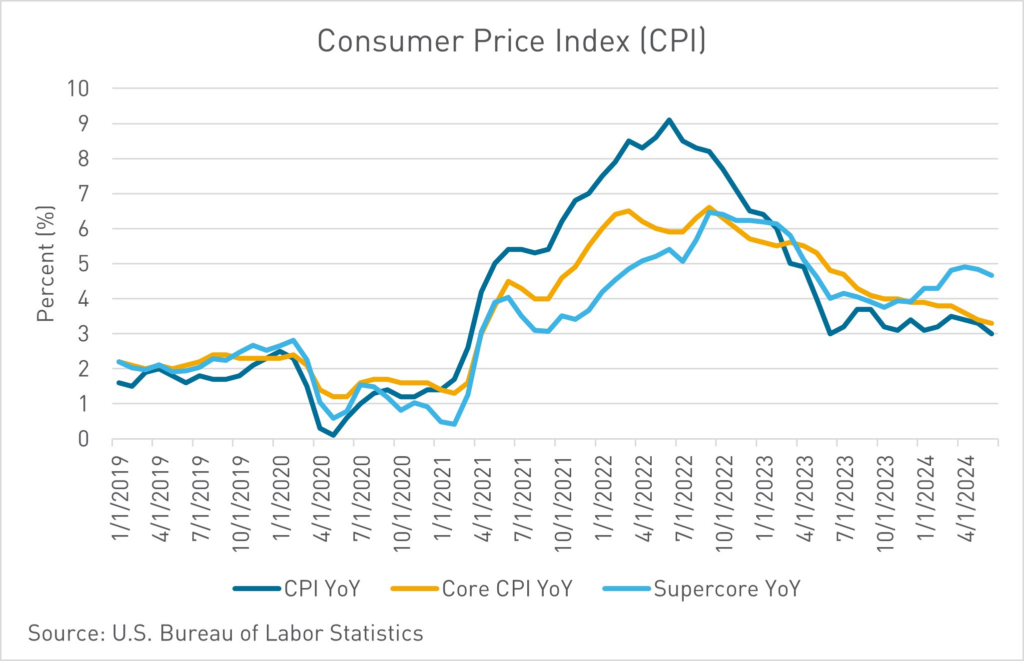

- June CPI print beats market expectations to the downside

- Shelter costs finally turn the tide in the CPI basket

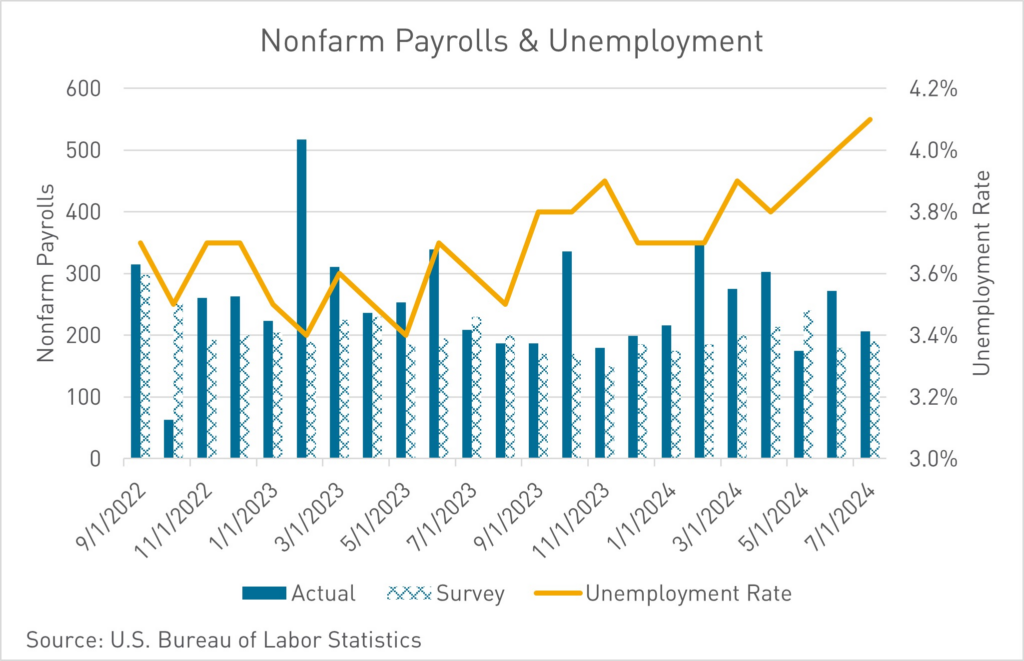

- Powell testifies to U.S. Senate that the FOMC has a keen eye on the labor market

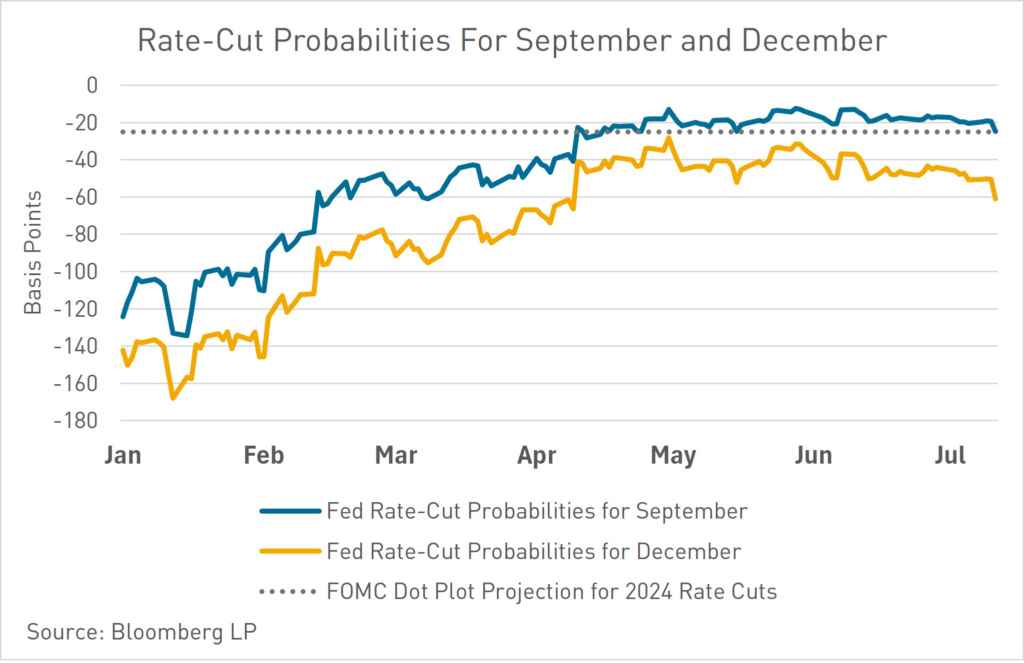

- Market expectations for a September rate cut continue to climb

The Federal Reserve is one step closer to achieving the Goldilocks scenario of a soft landing. On Thursday morning the U.S. Bureau of Labor Statistics released the June Consumer Price Index (CPI) figures. While annual numbers were roughly in line with expectations, the monthly number of -0.1% stole the show, with deflation headlines quickly appearing. While the headline YoY CPI numbers for June of ’23 and June of ’24 are identical, giving succor to the Fed is the fact that Core CPI over the same period fell from 4.8% last year to 3.3% this year. The move lower was largely buoyed by shelter costs registering their smallest increase since 2001. This CPI print has boosted investors’ hopes that the Federal Reserve could soon start cutting interest rates, with all eyes on the September FOMC meeting.

“Probably the most significant aspect of the June report is the downshift in housing inflation,” said Julia Coronado, the founder of MacroPolicy Perspectives LLC and former Fed economist. “It looks broad-based, and durable, and numerous Fed officials have indicated a downshift would boost their confidence that inflation is indeed returning to 2% in a sustainable way.” Services like airfares, hotel rates and inpatient hospital care all declined from a month earlier, in addition to slower rent increases. The costs of other new and used vehicle prices led broader decreases in the core goods basket.

The CPI print was released days after Fed Chair Jerome Powell gave testimony to the Senate Banking Committee. Powell noted in his testimony that a further cooling in the labor market could be undesirable. This comment was an important shift from the Fed’s laser focus on inflation, and implied that the FOMC may be closer to cutting rates as the unemployment rate moves higher. “Elevated inflation is not the only risk we face,” Powell said. “We’ve seen that the labor market has cooled really significantly across so many measures.…It’s not a source of broad inflationary pressures for the economy now.” Powell avoided signaling the timing of likely rate cuts and again insisted policy moves would be guided by incoming data. “We are sufficiently confident — even if the Fed is not yet ready to admit they are — that inflation is on the way back to the 2% target,” Joseph Brusuelas, chief economist at RSM US LLP, said in a note. “The road is now open to a rate cut by the Federal Reserve in September.” Powell’s comments on the labor market are notable following a recent uptick in unemployment, which is now at the highest level since 2021.

Despite Powell’s restraint in commenting on the timing of future rate cuts, the market is pricing in a strong probability of the first-rate cut coming at the September FOMC meeting. The market odds of a September rate cut rose from 65% to 91% following this week’s CPI print. Treasury bonds rallied reflecting this shift in probability, as yields fell 11 bps intraday on Thursday across the curve. The market will be focusing on Powell’s remarks at the July meeting, the only meeting between now and September, to see if Powell will tip his hand to signal a rate cut in September.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.