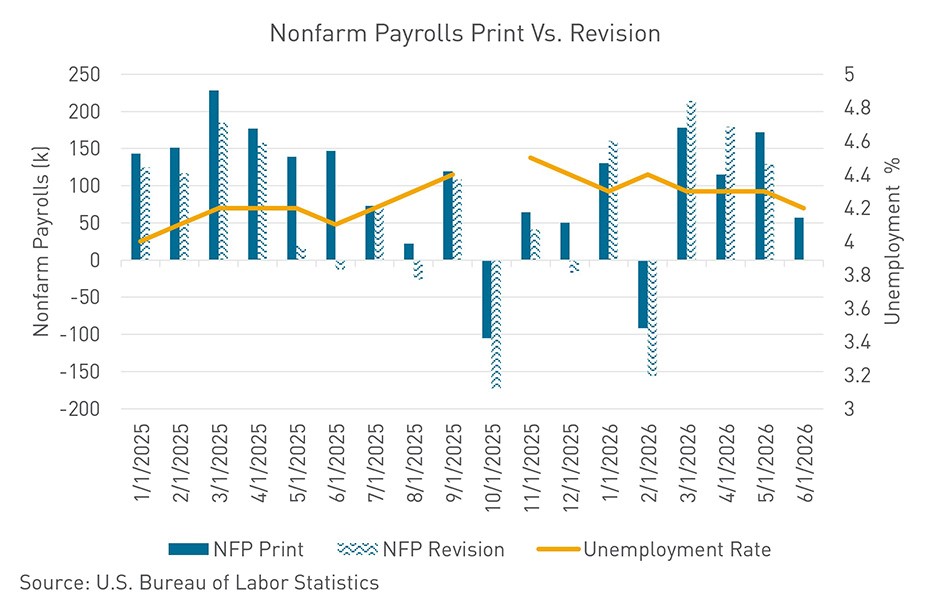

- June nonfarm payrolls increased by 57,000, well below expectations and accompanied by downward revisions to prior months.

- The unemployment rate declined to 4.2%, though much of the improvement was driven by a drop in labor force participation rather than stronger hiring.

- Hiring momentum has clearly moderated from the stronger pace seen earlier this year, but the data stops short of signaling a material deterioration in labor market conditions.

- Chair Kevin Warsh continues to emphasize incoming data over explicit policy guidance, increasing the market importance of each major economic release.

After three consecutive months of stronger-than-expected payroll growth, June finally delivered a downside surprise. Employers added just 57,000 jobs during the month and prior months were revised lower, taking some of the shine off what had looked like a meaningful reacceleration in hiring.

Headline unemployment rate improved to 4.2%, but the details were less encouraging. Labor force participation fell sharply, meaning the decline in unemployment was driven more by people leaving the labor force than by stronger employment growth. Even with the weak headline number, this does not look like a labor market that is breaking down. Hiring has clearly slowed from the pace seen earlier this year, but layoffs remain contained and overall employment growth continues to hover around levels that are generally consistent with a stable labor market. That’s an important distinction because markets continue to debate whether the economy is simply cooling or moving toward something more concerning. Today’s report supports the former.

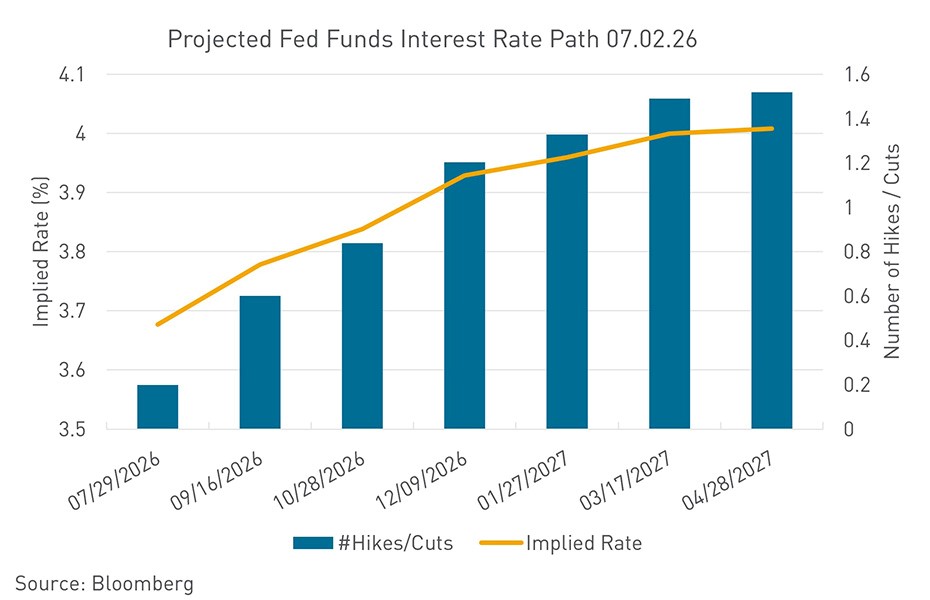

Treasury yields moved lower immediately following the release as investors reduced expectations for additional near-term tightening. Even after today’s rally, however, markets continue to price the possibility of further rate hikes later this year. That tells you everything you need to know about where investors believe the Fed’s focus remains: the labor market may be losing some momentum, but inflation is still the bigger problem.

That reality has become even more important under Chair Warsh. While previous Fed leadership spent considerable effort signaling future policy intentions, Warsh has made it clear that the committee intends to place greater weight on incoming data and less emphasis on providing a detailed roadmap. As a result, markets are increasingly being forced to react to the data itself rather than Fed guidance about the data.

For now, today’s report probably takes a July rate hike off the table. It does not, however, meaningfully alter the broader policy conversation. One softer payroll report is unlikely to outweigh inflation that remains above target, especially with energy markets and geopolitical developments still capable of creating additional price pressure.

The bottom line is that hiring has cooled, but one payroll report is not a trend. After several months of upside surprises, markets had begun to assume labor market strength was becoming more durable. June’s report serves as a reminder that the data remains uneven, and that month-to-month volatility can still distort the broader picture. While hiring momentum appears to have slowed, inflation remains the more important variable for both the Fed and interest rates.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.