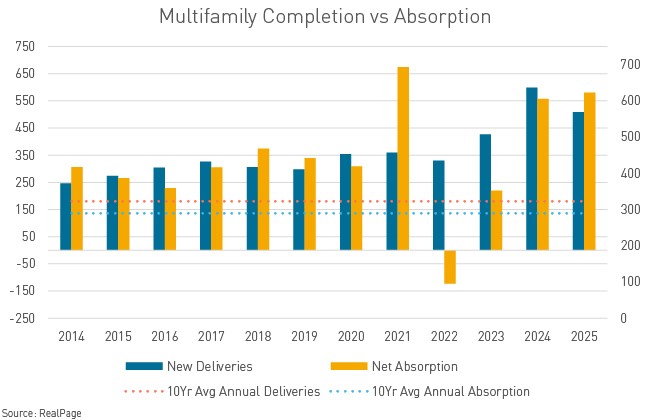

• Absorptions projected to outpace completions in 2025

• Cap rates are beginning to compress as vacancy rates fall

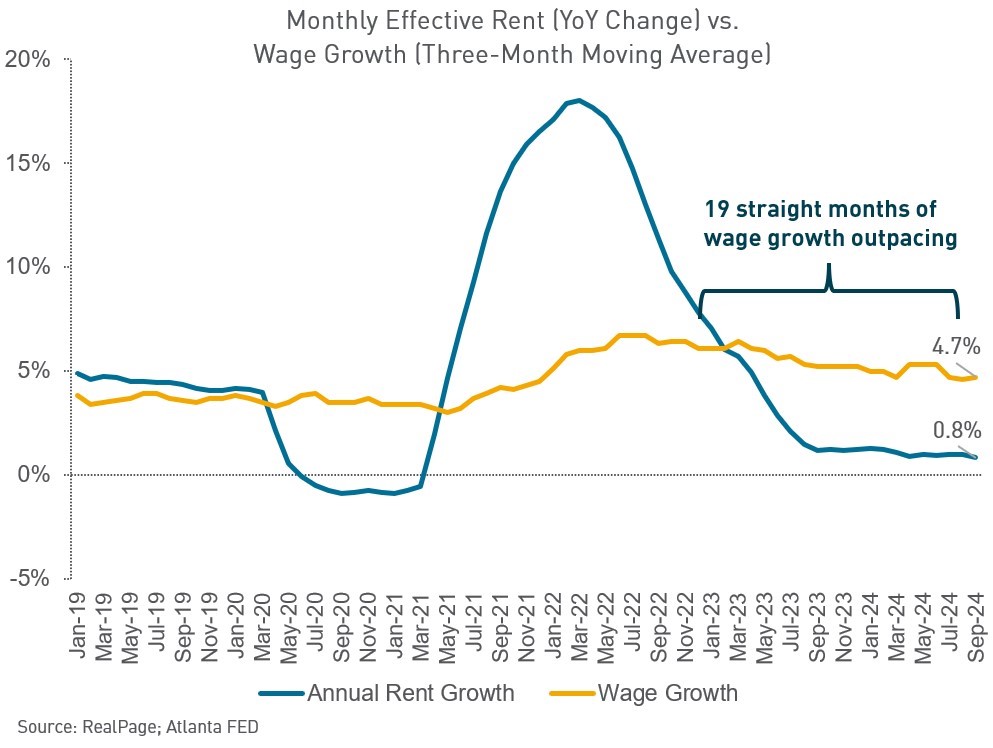

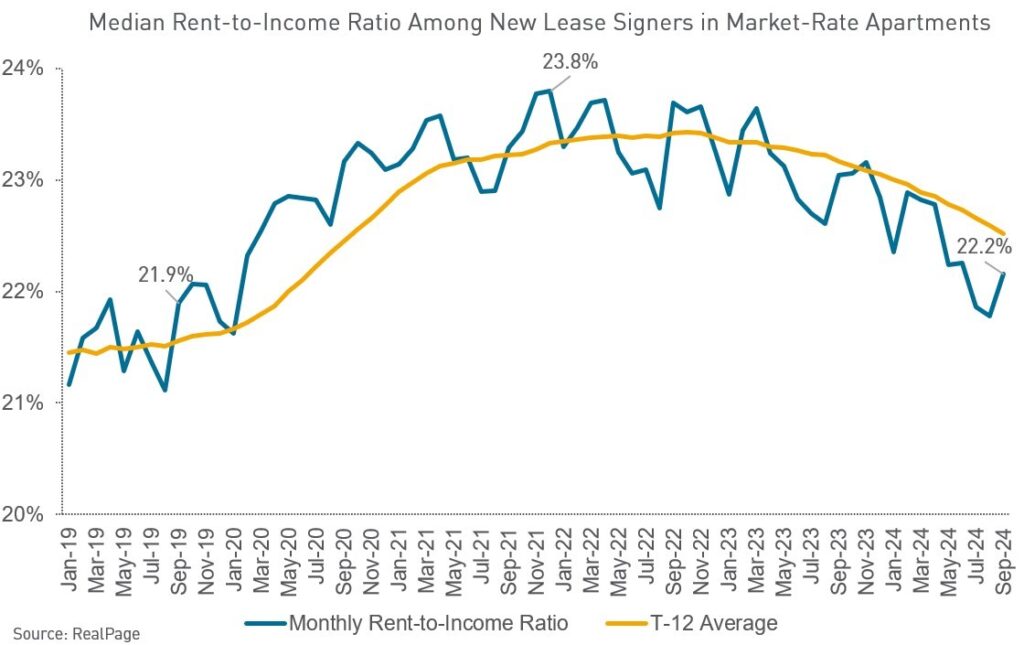

• Stagnant rent growth set to uptick as wages continue to increase

U.S. multifamily fundamentals have been stuck in a lull for nearly two years, but we are finally beginning to feel some tremors. The biggest apartment construction boom in decades flooded the market with new supply, while new deliveries have significantly outpaced net absorption. As renters have had strong pricing power over the past two years, effective rents of multifamily properties have been stagnant since January of 2022. This dynamic seems to finally be flipping; unit absorptions are projected to outpace deliveries in 2025. Vacancy rates decreased in Q3 24, which was the first vacancy decrease in three years, according to CoStar. The 1.2 million new apartment units that were built during the past two years are filling up. If rental demand is sustained and new deliveries lag behind absorptions, multifamily operators likely will have more pricing power starting sometime next year.

Multifamily operators are reacquiring pricing power at a time when renters are in a strong financial position; wage growth has outpaced rent growth since January of 2023. This recent growth in wages, paired with stagnant rent growth, has decreased the average rent-to-income ratio to the lowest level since early 2021. Increased return-to-office orders in major employment hubs may also start translating into higher rental demand, especially in coastal cities.

Demand for multifamily housing is projected to continue due to the current state of the single-family housing market. As noted in multiple Beyond Insights pieces, the single-family housing market is at the least affordable level seen in decades. After the refinance boom of 2021-2022, 84% of mortgaged homes had a rate with a 5% handle or lower, whereas current rates are closer to 7%. The average asking price of a single-family home skyrocketed during the pandemic. Those higher prices, paired with high mortgage rates, have created a financially unattractive mortgage payment when compared to the median asking rent.

As we look out to 2025, it feels the market is beginning to make a clear delineation between the two ends of the yield curve, indicating the phrase “rates are coming down” no longer universally applies. There is a high correlation between single-family mortgage rates and the 10-year Treasury. With many projections for 10-year Treasury yields hanging above 4.0%, single-family supply is likely to remain light over the next 12 months. And with so many other fundamentals in support of a rental rebound, there is cause for optimism as we head into the holiday season and turn our gaze to 2025.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.