- The FOMC held rates steady, signaling that further easing is contingent on renewed inflation progress

- Updated Summary of Economic Projections showed higher near-term inflation expectations

- Rising energy prices have re-elevated inflation risks, reinforcing the Fed’s pause

The Federal Open Market Committee held its March meeting on Wednesday, March 18, providing the market with forward guidance when it needed it most. Prior to the meeting, analysts were navigating a macroeconomic environment with both sides of the Fed’s dual mandate under pressure. Recent Personal Consumption Expenditures (PCE) and Consumer Price Index (CPI) prints showed lingering signs of upward price pressures caused by tariffs. Furthermore, inflation fears have been exacerbated by the recent jump in oil prices driven by the conflict involving Iran. At the same time, the labor market has shown signs of weakness, highlighted by a decline of 92,000 in the February nonfarm payrolls report. Against this backdrop, Powell acknowledged heightened geopolitical uncertainty but made it clear that restoring price stability remains the Fed’s priority, signaling that further rate cuts will require renewed progress on inflation.

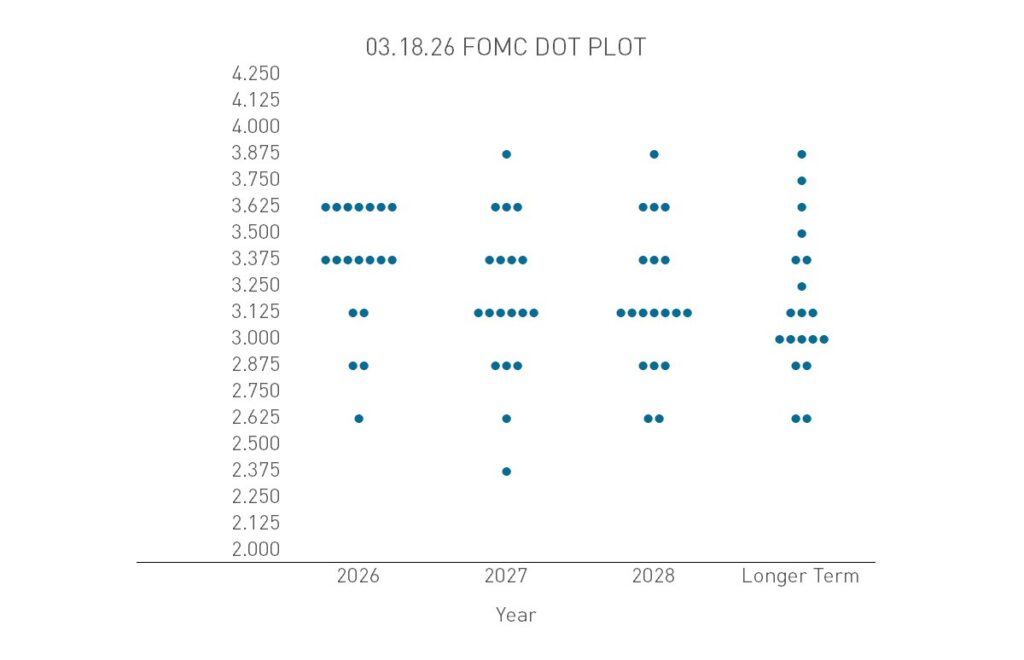

The Federal Open Market Committee (FOMC) voted 11–1 to hold the benchmark rate in the 3.50%–3.75% range. Fed Governor Stephen Miran dissented in favor of a quarter-point rate cut. The Fed’s “dot plot” of rate projections shows that the median official expects to lower rates by a quarter point in 2026 and another quarter point in 2027, unchanged from the projections released in December.

In the Summary of Economic Projections, the median Fed official sees core inflation rate at 2.7% by the end of 2026, up from 2.5% forecast in December. The growth outlook was revised modestly higher, with GDP projected at 2.4% versus 2.3% previously. Powell noted that if there were any meeting to skip providing economic projections, it would’ve been this one—the uncertainty of the duration and macroeconomic implications of the conflict involving Iran leave forward projections with a very short shelf life.

The core focus of the meeting was the inflationary impact of the conflict involving Iran through higher oil prices. Powell acknowledged that near-term inflation expectations have risen alongside energy prices and that higher oil will lift headline inflation in the short run. While the Fed typically looks through energy-driven price spikes, Powell stressed that this episode is more complicated given the backdrop of elevated goods inflation from tariffs. In that context, the energy-price shock is not occurring in isolation and therefore cannot simply be ignored.

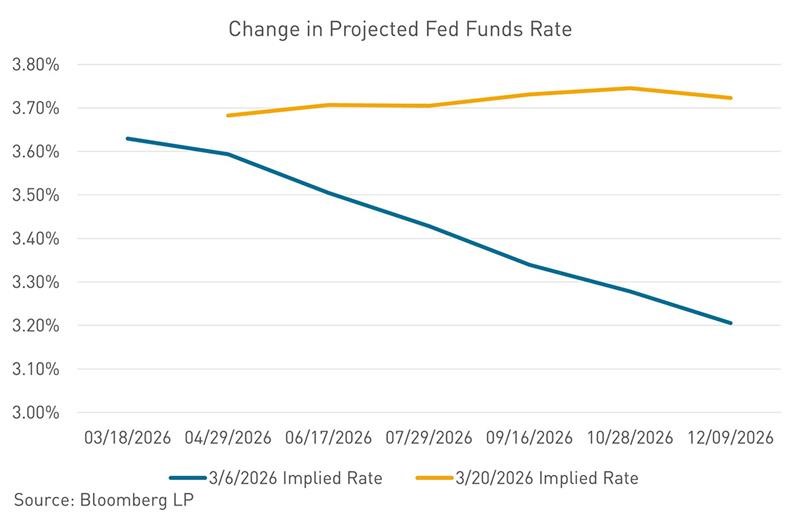

Taken together, the messaging made clear that inflation—not the labor market—is now the binding constraint on policy. While the Fed still expects inflation to ease as tariff effects roll off later this year, future rate cuts are explicitly conditional on that progress materializing. Absent clearer disinflation, policy remains on hold. For markets, this effectively ties the path of rates to energy prices, and Treasury markets sold off significantly on Friday as turmoil in the Strait of Hormuz continued. Bloomberg’s World Interest Rate Projection function now shows a higher probability of a rate hike in 2026 than the chance of a rate cut.

Powell provided a rare and unprompted comment on his future as Fed chair, signaling a willingness to remain in place if necessary to ensure continuity. He indicated that if Kevin Warsh is not confirmed by the Senate before Powell’s term expires in May, he would continue serving in a pro tem capacity, consistent with past precedent at the Fed. Powell added he would not step down from the Fed while the Justice Department investigation into the Fed’s building renovation project—and his testimony on the issue before Congress last year—is ongoing. Notably, Republican Senator Thom Tillis has said he will not vote to confirm Warsh until that investigation has concluded, effectively bottling up Warsh’s nomination in the Senate. Powell also stated that he has not yet decided whether he will serve out his term as a Fed board member through January 2028.

Powell closed by pushing back on comparisons to the 1970s. While acknowledging growing tension between the Fed’s inflation and employment objectives, he argued that the current backdrop lacks the entrenched inflation and policy missteps that defined the stagflation era, reinforcing the view that this is a difficult, but still manageable, policy challenge. The bottom line is that until inflation expectations cool and energy stops doing the inflation work, the Fed will stay paused.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.