- July CPI print shows moderate increase in inflation, particularly in services.

- July PPI print increased by the highest margin in three years.

- Bessent calls for 150 bps of interest rate cuts; other Fed governors say it’s too early to tell.

The United States’ macroeconomic landscape was reshaped in early August upon the release of the July nonfarm payroll and unemployment prints. The nonfarm payrolls print for July missed analysts’ projections to the downside, while the prior months’ figures were revised significantly lower. The weak figures portrayed an ailing labor market—the market promptly accelerated the expected timeline for the Federal Open Market Committee (FOMC) to resume cutting rates. The figures were the first of four labor market and price gauges the Fed had to consider between the July and September FOMC meetings; the second data point was the July Consumer Price Index (CPI) print.

The July CPI figure, released on Tuesday, had headline CPI unchanged from the prior print at 2.7% year over year. Core CPI, which excludes food and energy costs from the headline figure, rose at the fastest monthly pace since January. The key driver of the increase was an uptick in services prices, notably airfares as well as cars. Inflation for the goods most exposed to President Trump’s tariff policies slowed month over month. On a year-over-year basis, the core increased to 3.1% versus 2.9% prior.

The CPI figures largely met market expectations. For the Federal Reserve, the absence of a significant surge in CPI pressures likely eases the path to reducing rates in order to address concerns about a slowing labor market. Earlier this year, Fed officials noted that substantial tariff hikes might drive up prices, fueling inflation fears. Not all inflation measures have been immune to tariff price pressures, causing a general lack of clarity for the Fed.

The July Producer Price Index (PPI) was also released this week, and this print told a different story than the CPI figures. Wholesale prices, the cost of goods and services purchased directly from producers, rose at the sharpest monthly rate in three years, raising fresh alarm that tariffs are taking root in the economy and pushing up inflation. The producer price index increased 0.9% month over month, with services costs increasing 1.1% and goods prices excluding food and energy rising 0.4%. The report indicates companies are adjusting their pricing of goods and services to help offset costs associated with higher U.S. tariffs, despite the softening of demand in the first half of the year.

Demonstrated by the two dissenting votes at the July FOMC meeting, Fed officials are split on the future of monetary policy. Following the recent labor market and inflation prints, U.S. Treasury Secretary Scott Bessent urged the Federal Reserve to begin cutting rates. Bessent suggested that overnight rates should be at least 150 basis points lower than the Fed’s current benchmark. He proposed starting with a 50-basis-point cut in September, citing revised labor market data that might have influenced earlier rate decisions. Bessent said officials might have cut rates if they’d been aware of the revised data on the labor market that came out after the latest meeting, and he suspects rate cuts could have happened in June and July. Bessent’s comments mark a departure from the typical reluctance of Treasury secretaries to comment on Fed policy.

In an interview on Thursday, Federal Reserve Bank of St. Louis President Alberto Musalem took the opposite side of Bessent—Musalem said that it’s too early for him to decide on whether to lower interest rates at next month’s meeting. Musalem noted a 50 bp cut would be “unsupported by the current state of the economy and the outlook for the economy” from his perspective. Musalem is weighing the possibility of more persistent inflation against downside risks for the labor market, and said policymakers need to follow a balanced approach when there is tension between their mandated goals.

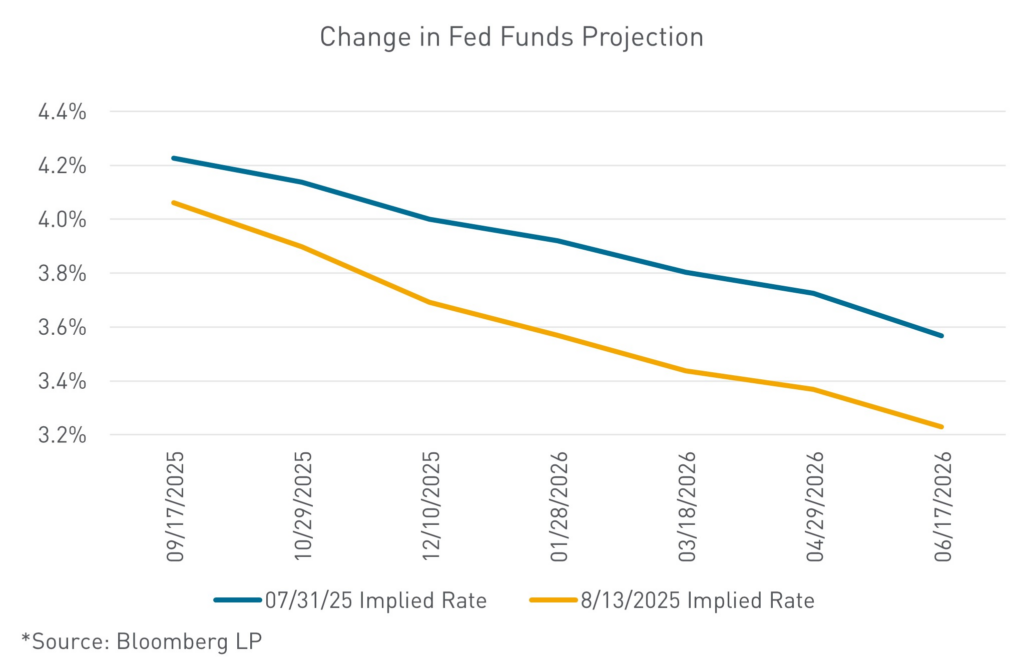

As we look ahead to the Federal Reserve symposium next week in Jackson Hole, where we anticipate updated guidance from Chair Powell, it’s important to contrast the recent CPI and PPI numbers. While the CPI print shows a moderate increase in inflation, particularly in services, the PPI print has increased by the highest margin in three years. This divergence, coupled with the Fed’s focus on unemployment rate rather than nonfarm payrolls, adds to the uncertainty surrounding the future path of rate cuts by the Federal Reserve. Additionally, President Trump has named 11 possible successors to the Fed Chair, and interviews with these candidates may influence market expectations for monetary policy. With four new voting members joining the FOMC next year, the makeup of monetary policy will also change. Despite the levels of uncertainty and volatility, the bull steepening of the yield curve and futures markets odds indicate two cuts this calendar year.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.