- Agency lending is starting to hit its stride, with volumes starting to increase on a monthly basis

- Third-party capital is broadly available, but flexibility, structure, and certainty are being explicitly priced

- Investment sales activity is concentrated in higher-quality assets as buyers remain disciplined

The key theme of the Commercial Real Estate (CRE) lending space to start the year was the abundance of liquidity. The Federal Housing Finance Agency (FHFA) raised the Agencies’ caps to $88B. Debt funds were abundant with multifamily-specific capital to lend, and life companies had fresh allocations. To start the year, the Agencies were competitive but disciplined; neither Fannie Mae nor Freddie Mac was in chase mode despite strong year-to-date volume.

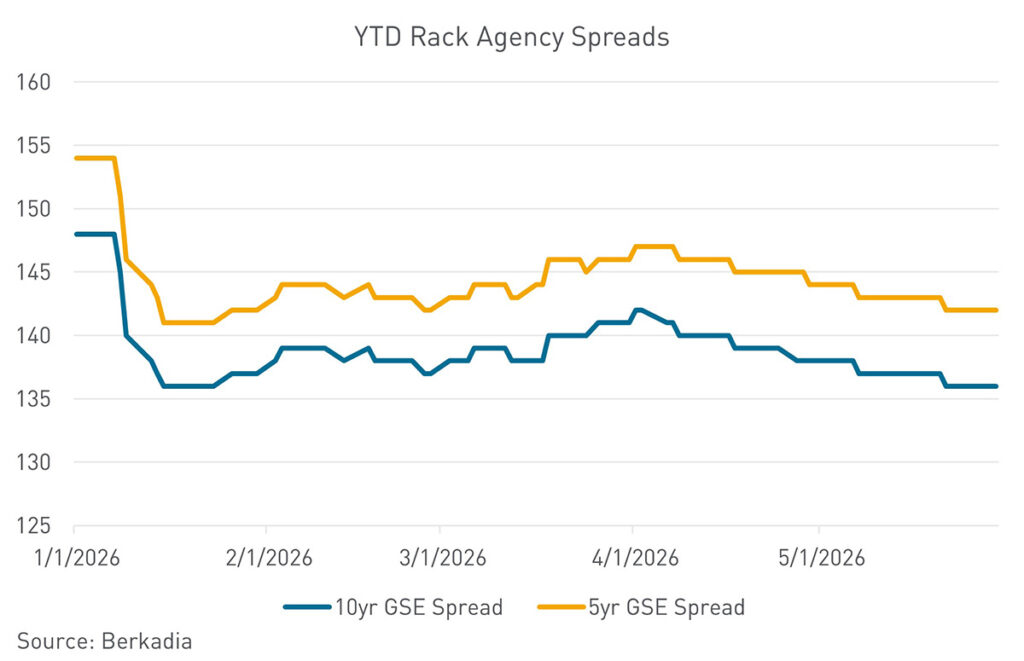

Agency Commercial Mortgage-Backed Securities (CMBS) trading spreads have performed well year to date. Spreads widened slightly in March due to market uncertainty surrounding the conflict in Iran but have since rebounded to YTD tights. Constant volatility in the treasury market has curbed trading volumes, particularly since the start of the Iran conflict. The lack of volume has provided a tailwind for trading spreads to tighten, and strong investor demand is not being met by current origination volumes, driving spreads tighter. Deals with full-term interest-only structures, or those that utilize a rate buydown, currently have the strongest market demand, and trade at the tightest spreads.

Year to date, debt fund activity has remained strong. In the securitized market, a bifurcation persists between conduit and Single-Asset, Single-Borrower (SASB) execution, particularly around pricing, execution certainty, and investor demand, with SASB continuing to attract stronger interest. At the same time, the debt fund market has been more volatile over the last 30 to 45 days, with frequent retrades late in the closing process, often ranging from 15 to as much as 50 to 60 basis points, highlighting the continued fluidity in that segment, and reinforcing that execution certainty remains a key consideration through closing.

Another notable theme, thanks to the availability of debt liquidity, is a broader lender outreach, particularly across debt funds and life companies, suggesting a more cautious and exhaustive approach to capital formation than in prior periods. As a result, activity continues to skew toward shorter-term opportunities while the team is evaluating ways to generate more traction, potentially by including preferred equity quotes alongside Freddie executions so borrowers can better assess the option.

Debt markets remain highly liquid, with aggressive spreads and a broad set of lenders actively pursuing refinancings and originations, while investment sales momentum continues to build. That said, transaction activity is still concentrated in higher-quality assets, as buyers remain disciplined, underwriting to durable income and clear NOI growth rather than speculative rent assumptions. Multifamily fundamentals are improving in select markets, supported by household formation, affordability constraints in homeownership, and stronger absorption in certain areas, but the recovery remains uneven by market and submarket. As a result, location, asset quality, and vintage continue to be critical differentiators. While investor sentiment is mixed, significant capital remains available for the right opportunities, particularly in the core-plus segments, so long as downside protection and risk-adjusted returns are clear.

Market activity remains constructive despite ongoing volatility. Recent market examples reinforce the themes of selective but deep capital availability and continued consolidation: there is massive interest in the $1.6 billion Camden California portfolio, underscoring strong demand for scaled, institutional-quality product, even without a clear portfolio premium. In addition, the announced merger between AvalonBay and EQR highlights the ongoing consolidation trend among public REITs as firms seek scale, operating efficiencies, and future growth avenues such as affordable housing.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.