College enrollment is essential to the health of the student housing market, among the most important subsectors of the multifamily industry. However, the latest findings from the National Student Clearinghouse (NHS) Research Center confirmed that enrollment at secondary institutions continues to decline. Through spring 2019, year-over-year enrollment nationwide has fallen 1.7%.

What’s behind this latest shift in enrollment? The factors driving the trend are multifaceted:

- Expanding Economic Opportunities – Traditionally, enrollment increases during periods of economic instability—such as during a recession—and decreases during periods of improving economic activity. As this has been the case in the United States over the last several years, college enrollment has predictably slowed.

- Declining National Birth Rates – One of the most basic factors that influences enrollment is the number of people most likely to attend college—those between the ages of 18 to 35. Various factors have spurred a gradual decline in the total birth rate starting in 2009 and led to a record-low 1.73 average lifetime births per woman in 2018, according to the U.S. Centers for Disease Control and Prevention.

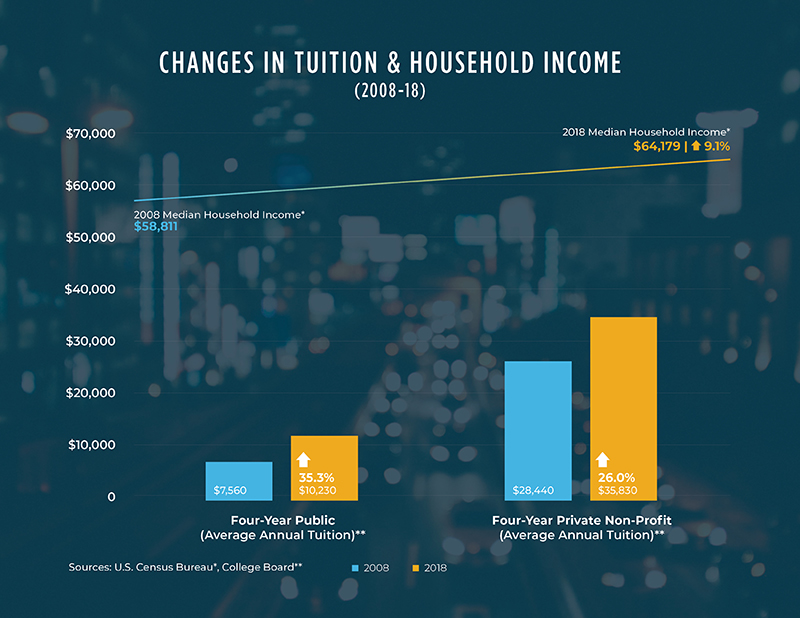

- Rising Tuition Costs – The simple reality is that income growth for most Americans has trailed the rapidly increasing cost of college tuition. While household median incomes expanded by over 9% from 2008 to 2018, the cost of annual tuition rose nearly three times as quickly. Over the same period, four-year public institutions increased tuition over 35%, while tuition at private/non-profit colleges rose 26%, according to the College Board.

For-Profit Schools Struggling to Justify ROI

After posting low graduation rates and more than double the number of students defaulting on their school loans, many for-profit schools have begun shuttering across the country. Those schools that remain will face challenges in changing increasingly negative perceptions and replenishing shrinking student bodies. Overall, college enrollment at for-profit schools has been on the decline since 2010, limiting opportunities for nearby multifamily development.

The same NHS report that showed enrollment declining annually 1.7% also revealed that the drop-off was concentrated at private/for-profit universities. Since spring 2018, annual enrollment at four-year private/for-profit schools dropped 19.7%.

Conversely, enrollment at four-year public universities fell by only 0.9%. Enrollment at four-year private/non-profit institutions increased by 3.2%, gains driven in part by successful former for-profit schools converting their operations to non-profit models.

Top Public Schools Still Driving Demand

While overall enrollment at four-year public universities has declined, enrollment at top-performing public universities has actually increased, especially if those universities are located near a booming metro with a growing economy.

“If job growth remains positive, unless there is a substantial restructuring by employers to put less weight on the value of a college degree for new hires, we expect enrollment to continue to grow,” said Senior Director Greg Gonzalez, in a recent Q&A with Berkadia.

In the same interview, Senior Director Kevin Larimer emphasized, “Even where enrollment is static, if supply has not been overbearing, the market will remain healthy.”

Case in point: Consider Georgia State University and Kennesaw State University, two of the three largest public universities in the state of Georgia. Both schools set overall enrollment records during the 2019-2020 school year, increasing total enrollment by 1.5% and 6.7%, respectively.

Both schools are located in the Atlanta metro area, a market that boasts rent growth and job growth that are better than the national average as well as a healthy construction pipeline with 12,000 new multifamily units scheduled to come online before the end of 2020.