Last month was dominated by chatter about trade wars, potential recessions, and interest rate adjustments by the Federal Reserve. Plenty of experts are making sour predictions about the future of the economy, so it was easy to overlook the substantial body analysis released in August that suggests the opposite. In fact, the numbers suggest that multifamily may be uniquely prepared for the next big shift in monetary policy.

1. Analysts Expect Minimal Short-Term Impact from Fed Cuts

Optimistic analysts feel confident that the commercial real estate industry is largely insulated from potential impacts of federal interest rate cuts. In fact, the industry may even benefit as rate cuts encourage borrowers to reevaluate the upside of commercial mortgage-backed securities (CBMS) compared to other sources of capital:

- “The CMBS market competes against other lending institutions, insurance companies, hedge funds and so forth,” said Trepp Senior Managing Director Manus Clancy. “Because of [insurance companies’] actuarial needs, they really hate to lend under 4%. The CMBS market doesn’t really care where absolute rates are, so sometimes you see insurance companies forfeiting [market] share because rates get too low.” – Bisnow

2. Lower Interest Rates Won’t Hinder Multifamily Demand

Interest rate cuts have contributed to making housing more affordable, but multifamily investors have no reason to fret. Key factors such as millennial lifestyle trends and an abundance of student loan debt suggests the preference toward renting isn’t changing anytime soon. Despite an uptick in mortgage refinancing, there’s a long list of reasons, economic and cultural, that all but guarantee that the multifamily revolution is here to stay:

- “House prices have been rising where they’re already unaffordable and falling where they’re within reach. To put it another way: If you want to make a good investment, you can’t afford it; if you can afford it, it’s not going to be a good investment.” – Axios

3. Borrowing Volume Up, Banks Soften Long-Term Lending Standards

Mortgage originations for commercial and multifamily real estate have performed especially well during the first half of 2019. Quarterly analysis performed by the Mortgage Banker Association (MBA) showed that mortgage originations increased over the previous year. Furthermore, originations in the second quarter handily outpaced the first quarter by 29%. This trend is just another sign of long-term stability in the multifamily industry:

- “Originations for life insurance companies and for Fannie Mae and Freddie Mac continued at record paces during the first half of the year, as did originations of loans backed by multifamily and industrial properties,” said MBA Vice President Jamie Woodwell. “With rates even lower during the third quarter, absent a major economic disruption, 2019 is shaping up to be another record year for commercial mortgage lending.” – Housingwire

An even better sign of confidence for the multifamily industry? The most recent U.S. Federal Reserve quarterly survey suggests that loan standards for commercial and industrial loans are expected to ease or remain stable over the foreseeable future:

- “The survey showed demand for commercial loans from larger firms in the second quarter was mostly unchanged, but the details suggest an improvement: among the minority reporting a change in demand, there was a decline in the portion seeing a weakening, and an increase in those seeing strong demand, compared with the first quarter.” – WKZO

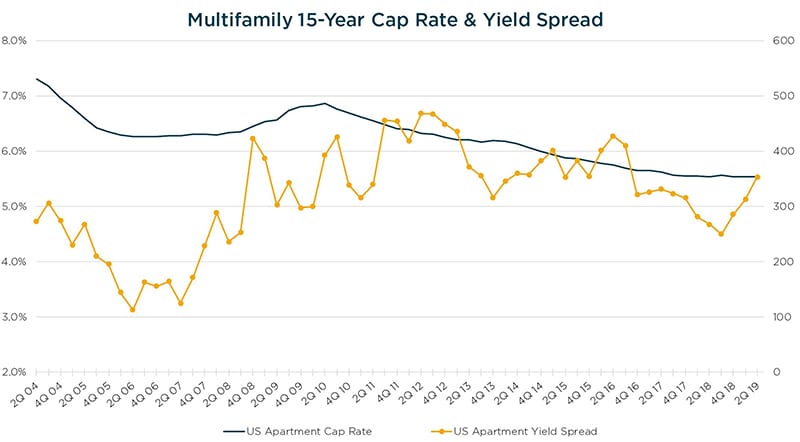

4. Cap Rates and Yield Spread Suggest Stability in Multifamily

Overall, multifamily cap rates remained stable at 5.5% through the first half of 2019. Despite cap rates tightening over the past five years, the current spread between the average cap rate and the 10-year treasury remains in-line with the historical average of 327 bps (2002-2019).

This development should give investors confidence that there is still room for price growth within the multifamily market. Investors should look at secondary markets as an alternative to the high-end, Class A properties found in coastal markets where cap rates trend to be in the sub 4.0% realm:

- “Cap rate spreads between Class A and Class B, and between Tier I and Tier II markets, remained tight. This suggests that some investors are trading class for value, finding better opportunities in lower-quality assets as well as in secondary and tertiary markets.” – RE Journals