- Iran announced the Strait of Hormuz is fully reopened to commercial traffic, triggering a sharp decline in oil and natural gas prices

- While energy markets are easing, the prior supply shock has already filtered into inflation data and will remain relevant for the Fed

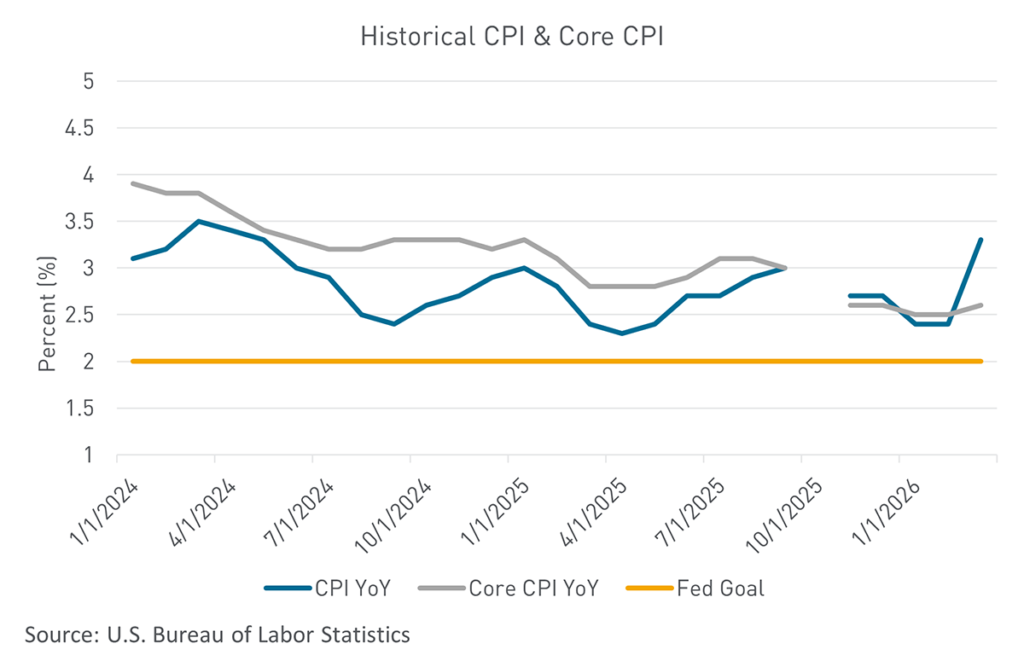

- Last week’s CPI print and softer consumer spending data reinforced a stagflation-lite backdrop heading into the next FOMC meeting

Markets received long-awaited relief Friday morning after Iran announced that the Strait of Hormuz was “completely open” for commercial vessels—a development that immediately unwound some of the largest geopolitical risk premium embedded in global energy markets. The move marks an important de-escalation after nearly seven weeks of extraordinary volatility. Since late February, the closure of the Strait had disrupted roughly one-fifth of global oil flows, sending crude sharply higher and creating immediate downstream pressure on gasoline, diesel, freight, aviation fuel, and industrial input costs. Even with the reopening announcement, markets are now confronting a familiar macroeconomic reality: financial conditions can ease quickly, but inflationary pass-through lingers.

The reopening of the Strait removed the left-tail risk scenario: a prolonged choke point in the world’s most important energy corridor. That risk premium is now unwinding rapidly; markets are effectively pricing that the war is moving from escalation toward negotiation. Friday’s oil selloff was significant, but crude remains materially above pre-war levels—brent futures are still roughly 20% above where they traded before the conflict began.

For the Federal Reserve, the reopening of Hormuz was welcome news but not a clean policy escape hatch. The central bank now faces a sequencing problem: the market shock may be fading just as the inflation data begins to show its full effect. Prior to Friday’s announcement, the Fed had already shifted into a holding pattern. Stronger payroll data earlier this month removed urgency to cut rates on the employment side of the dual mandate, while the oil shock raised renewed doubts that inflation would continue gliding lower. Fed Chair Jerome Powell stated earlier in the month that longer-term inflation expectations appear to be well anchored and characterized the Fed’s current policy stance as content to wait and see. The Fed’s default tendency is to look through energy-driven price spikes, treating them as temporary disturbances rather than structural inflation.

Friday’s energy reversal reduces the probability of a near-term upside inflation spiral, but it likely does not create enough confidence for immediate easing. Instead, it gives policymakers further reason to wait. If oil stabilizes lower and core inflation remains contained, cuts later this year can return to the table. If headline inflation feeds into expectations or wage demands, the pause extends. The most likely outcome remains unchanged: the Fed stays on hold until it has several months of cleaner inflation data.

Last week’s March Consumer Price Index (CPI) report exemplified the extreme impact an oil shock can have on inflation. Headline consumer prices surged 0.9% month-over-month, the largest monthly increase since 2022, pushing the year-over-year rate to 3.3%. Nearly three-quarters of the monthly rise came from gasoline prices alone. Core inflation, which removes volatile food and energy price measures, was more measured, rising just 0.2%. The inflation shock was driven primarily by energy rather than broad-based overheating demand. Services inflation also remained relatively tame, giving the Fed some room to look through the move—provided energy prices continue normalizing. At the same time, real consumer spending in February rose just 0.1%, while real disposable income declined 0.5%, signaling households were already under pressure before the March gasoline spike fully hit wallets.

The recent prints leave the U.S. economy in an uncomfortable but manageable place: growth is slowing, consumers are cautious, but inflation is still too high to justify aggressive easing. The reopening of the Strait of Hormuz is a clear near-term positive for markets, consumers, and policymakers alike. It lowers the probability of a more severe global supply shock and removes one of the largest macro tail risks confronting investors this spring. For the Federal Reserve, the damage from the initial shock has already been partially done—higher energy prices have flowed into headline inflation, weighed on sentiment, and complicated the path toward rate cuts. The geopolitical crisis may be easing faster than the monetary policy challenge it created.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.