- The Federal Reserve held rates steady, but the June meeting delivered a meaningfully more hawkish signal than markets expected.

- Updated projections showed higher inflation, slower growth, and a committee increasingly open to the idea of a 25 bp hike by year end.

- The Fed also signaled a shift away from forward guidance, giving markets less of a roadmap and placing greater emphasis on incoming data.

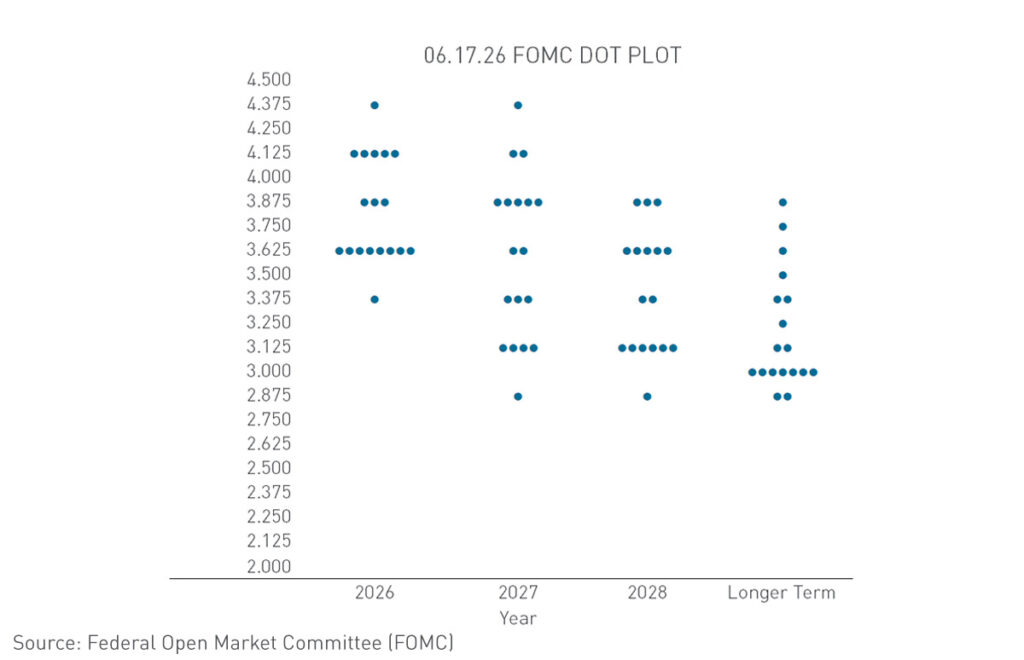

Everyone will focus on the missing dot.

The market sold off because of the nine that remained. Half the committee is now willing to discuss another rate hike this year, and that is a very different conversation than the one markets were having just a few months ago. Inflation forecasts moved higher, growth forecasts moved lower, and the Fed made clear that inflation remains the bigger concern.

Treasuries didn’t react to the revisions in the summary of economic projections themselves; they reacted to a policy outlook that looks less certain and potentially more restrictive than investors expected. The market came into the meeting looking for clues about the path to lower rates. It left the meeting debating whether the next move could still be higher.

The communication changes matter but probably not for the reason most people think. The shorter statement, removal of forward guidance, and Warsh’s decision not to submit a dot weren’t simply stylistic choices. They appear to signal a Fed that wants less emphasis on forecasting policy and more emphasis on responding to incoming data.

For years, markets became conditioned to looking at Fed communication for a roadmap. Warsh seems to be pushing the committee away from that approach. The message was less “here is where rates are going” and more “here is how we are thinking about the data.” That doesn’t necessarily make the Fed more hawkish, but it does make the path of policy less predictable.

And that’s where the dots become important. If the Fed is moving away from forward guidance, then the actual distribution of views inside the committee matters even more. The absence of one dot generated headlines. The presence of nine dots pointing to another hike moved markets.

For commercial real estate, the takeaway is straightforward. The assumption that rates would steadily drift lower in the second half became harder to support after this meeting. Treasury volatility is likely to remain elevated, and borrowers should be prepared for a Fed that is more data-dependent and less interested in providing advance notice of where policy goes next.

That said, Fed policy is not the only story driving markets right now. In the near term, rate movements may continue to be dictated more by developments in the Middle East than by anything that came out of the June Federal Open Market Committee (FOMC) meeting. The Fed changed the medium-term conversation. Geopolitical headlines may still determine tomorrow’s opening trade.

Everyone will talk about the missing dot. Markets moved because of the nine that remained. Just as important, Warsh appears to be steering the Fed away from forward guidance and toward a more data-dependent framework. That doesn’t tell us where rates are headed. It tells us the market is going to have to work harder to figure it out. However, in a market currently watching Iran as closely as inflation, the Fed may just be setting the backdrop while headlines drive the day-to-day volatility.

This commentary and any statements, information, data and content contained therein, and any materials, information, images, links, sounds, graphics or video provided in conjunction with this document (collectively “Materials”) has been prepared for informational purposes or general guidance on matters of interest only, and does not constitute professional advice, advertising or a solicitation. The Materials are of a general nature and not intended to address the circumstances of any particular individual or entity. You should not act upon the information contained in the Materials without obtaining specific professional advice. As such, nothing herein constitutes legal, financial, business, investment or tax advice and you should consult your own legal, financial, tax, investment or other professional advisor(s) before engaging in any activity in connection herewith. The information in the Materials is not a substitute for a thorough due diligence investigation. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in the Materials, and, to the extent permitted by law, Berkadia Commercial Mortgage LLC ( together with its affiliates, the “Company”) neither accept nor assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the Materials or for any decision based on them. No part of the Materials is to be copied, reproduced, distributed or disseminated in any way without the prior written consent of the Company.